Wealth Building Wednesday – Debt Management Strategies on Clint’s YouTube Channel.

Hey everyone, Clint here, bringing you this week’s episode of Wealth Building Wednesday, with some practical advice on managing debt. Here’s some quick tips on what works and what doesn’t in the realm of debt.

Good vs. Bad Debt: First things first, not all debt is created equal. There’s the kind that’s working for you, like investments in real estate that bring in more than they take out. Robert Kiyosaki likes to promote good debt as debt used to purchase assets. He describes assets as anything that brings you a return.

Then there’s the kind we’d rather avoid—high-interest culprits like credit card debts. It’s OK to have and use credit cards, but not to carry a balance on them. You should pay them off every month either when they are due or before they are due to ensure you don’t pay interest. This is a good strategy if you don’t have a balance or have paid off your balance. If you already have a balance on your credit card(s), see below how to eliminate them.

Mortgages can be a smart play if you’re investing in your future home, as long as you maintain the home and can expect decent appreciation. Even then, it will depend on what your interest rate is. If it is low, as in less than 5%, you may not want to pay off your mortgage, unless you would feel better not owing anything on your home.

Student loans are a mixed bag depending on what you’re aiming for career-wise, what type of loans you have, and again, what the interest rates are. Students should be informed on the expected ROI of their chosen degree program. The same degree program at different schools can range from a moderately positive ROI (165% or so) at one school to an extremely negative ROI (-450% or so) for a music education degree. This information was found here when researching in-state music education undergraduate degrees in Louisiana for my oldest daughter. The fact that Northwestern State University had the highest ROI for that degree and the largest amount of scholarships offered between, she will wind up with an almost infinite return for her degree.

Tackling the Debt Dilemma: We’ve touched on strategies like the debt avalanche and snowball methods before—both solid tactics depending on whether you want to hit the high-interest debts first or knock out smaller debts for quick wins. The goal? Eliminate your bad debt so you’re not bleeding money on interest and can focus on growing your wealth.

Why It Matters: Let’s be real…debt can be a drag on your financial journey, especially if it’s the kind that doesn’t give back. Shaking off that debt means more freedom to invest in your future, and that’s what we’re all about here.

Eliminating your debt will give you options…and thee who hath the most options, wins!

Got a question or a thought to share? Leave a comment or shoot me an email; I’m here to help or dig deeper if needed. And hey, if you found this chat helpful, why not share it with a friend?

Clint C. Galliano, a native of Lafourche Parish, has lived in the Houma-Thibodaux area for over 36 years and is currently a REALTOR® with Keller Williams Realty Bayou Partners in Houma, La. He has been involved with real estate investing since 2017 and hosts the local Real Estate Investment Association. Real Estate is his passion. Clint previously worked in drilling fluids and drilling fluids automation for 28 years. He lives in Bayou Blue with his wife and two daughters.

Clint C. Galliano, REALTOR® 985.647.4479 clint.galliano@kw.com Licensed by the Louisiana Real Estate Commission Keller Williams Realty Bayou Partners 985.262.4400 307 Bayou Gardens Blvd Houma, La 70364 Each Office is Independently Owned & Operated

Join us for an in-depth look at budgeting and its vital role in wealth building. Learn practical tips and strategies to take control of your finances and maximize your wealth potential.

Why Budgeting Is Essential for Wealth Building

Budgeting is not just about managing your expenses; it’s a strategic tool for achieving financial freedom and realizing your long-term goals. By carefully allocating your resources and making informed financial decisions, you can build a solid foundation for wealth creation.

The Power of Smart and Flexible Planning

Effective budgeting is not about penny-pinching or living a restrictive lifestyle. It’s about smart, flexible planning that empowers you to optimize your spending, prioritize saving, and make informed investment choices. We’ll explore real-world examples of how strategic budgeting can lead to significant wealth accumulation.

Leveraging Technology for Personalized Budgeting

Discover the benefits of using advanced tools such as Rocket Money, Pocket Guard, or Every Dollar for personalized expense tracking and budget management. We’ll highlight how these innovative platforms can help you identify opportunities for savings and align your financial journey with your lifestyle.

The Importance of Flexibility in Budgeting

We’ll delve into the significance of incorporating flexibility into your budget to prevent overspending and ensure a balanced financial approach. Learn how to avoid the pitfalls of tight budgets that may lead to impulsive splurges, and find out how to maintain a healthy balance between disciplined saving and guilt-free indulgence.

Mindful Spending and Consistent Saving

Budgeting isn’t just about restricting yourself; it’s about enhancing your life by cultivating mindful spending habits and maintaining a consistent saving regimen. We’ll provide practical tips for integrating budgeting into your daily life and maximizing its positive impact on your long-term financial well-being.

Engage and Transform with Debt Management

Get ready for our next episode, where we’ll tackle the complexities of debt management and help you transform daunting numbers into manageable financial milestones. Don’t miss this opportunity to gain valuable insights into effectively managing and overcoming debt.

Conclusion:

In conclusion, mastering the art of budgeting is the cornerstone of wealth building. Incorporating smart, flexible planning, leveraging innovative tools, and maintaining a balanced approach are key to achieving long-term financial prosperity.

Join us next week for an insightful exploration of debt management.

Remember, your active engagement and feedback are invaluable to our journey towards financial empowerment.

Clint C. Galliano, REALTOR® 985.647.4479 clint.galliano@kw.com Licensed by the Louisiana Real Estate Commission Keller Williams Realty Bayou Partners 985.262.4400 307 Bayou Gardens Blvd Houma, La 70364 Each Office is Independently Owned & Operated

Clint C. Galliano, a native of Lafourche Parish, has lived in the Houma-Thibodaux area for over 36 years and is currently a REALTOR® with Keller Williams Realty Bayou Partners in Houma, La. He has been involved with real estate investing since 2017 and hosts the local Real Estate Investment Association. Real Estate is his passion. Clint previously worked in drilling fluids and drilling fluids automation for 28 years. He lives in Bayou Blue with his wife and two daughters.

Below is an AI-generated summary of the video along with the transcript. You can also watch it here.

In an era where financial literacy has become a cornerstone of personal growth and security, understanding the fundamental concepts of wealth and net worth is not just beneficial—it’s essential. Drawing insights from a thought-provoking video on these subjects, this post aims to unravel the complexities of financial well-being, offering a fresh perspective on what it means to be truly wealthy.

Video Show Notes:

In this episode of Wealth Building Wednesday, we embark on a comprehensive exploration of the fundamental concepts of wealth and net worth. Clint emphasizes the goal of providing financial wisdom to cultivate a secure and prosperous future. The discussion underscores that wealth transcends mere monetary accumulation; it embodies a lifestyle abundant in opportunities and devoid of financial stress.

As the episode unfolds, the focus shifts to demystifying wealth and net worth. The narrative is geared towards unraveling these concepts to lay a solid foundation for financial empowerment. Through engaging explanations and insightful examples, viewers are guided through the nuances of financial health, investment strategies, and the principles of asset management.

The episode is designed to be an enlightening journey, encouraging viewers to rethink their approach to personal finance. It aims to equip the audience with the knowledge and tools necessary to navigate the complexities of wealth building, fostering a community of financially savvy individuals committed to achieving long-term security and success.

“Welcome to Wealth Building Wednesday, your weekly dose of financial wisdom to help you build a secure and prosperous future.

Today we’re diving into the essentials of understanding wealth and net worth. Let’s unlock the secrets to financial success together!

Hey Y’all! I’m thrilled to have you join us on this journey towards financial empowerment.

Wealth isn’t just about having lots of money; it’s about creating a life that’s rich in possibilities and free from financial worries.

So where do we start? With understanding wealth and net worth.

First off let’s clarify what we mean by ‘wealth.’

It’s not just your monthly paycheck; it’s the accumulation of valuable assets that provide financial security and freedom.

Now net worth—it’s a simple yet powerful concept.

It’s what you own minus what you owe. Assets like your home investments and savings minus any debts and liabilities.

Imagine a scale. On one side you have your assets and on the other your liabilities.

The goal? To tip the scale in favor of your assets. That’s positive net worth and it’s the foundation of wealth building.

Why focus on net worth? Because it’s the true measure of financial health. A positive net worth means you’re on the right track building a buffer against life’s uncertainties and paving the way for future wealth.

So how do we increase our net worth?

Start by paying down high-interest debt which eats away at your wealth.

Next boost your savings—aim to save at least 20% of your income.

And don’t forget about investing. It’s not just for the wealthy; it’s how the wealthy got there. Even small consistent investments can grow significantly over time thanks to the magic of compound interest.

Remember building wealth is a marathon not a sprint. It’s about making smart choices and staying committed to your financial goals.

And that wraps up our first episode of Wealth Building Wednesday. I hope you’re feeling inspired to take control of your financial future.

Join us next week as we tackle the art of budgeting for wealth. Until then keep striving for financial success.

Thank you for watching!

Don’t forget to like subscribe and hit the notification bell so you never miss an episode of Wealth Building Wednesday.

Share this with someone who could use a financial boost and let’s build wealth together. See you next week!”

Remember, if you have a real estate need, whether buying or selling, give me a call or shoot me an email. It doesn’t matter if you are outside of my area, I can connect you with a Rockstar Real Estate Agent!

Clint C. Galliano, REALTOR® 985.647.4479

Clint C. Galliano, a native of Lafourche Parish, has lived in the Houma-Thibodaux area for over 36 years and is currently a REALTOR® with Keller Williams Realty Bayou Partners in Houma, La. He has been involved with real estate investing since 2017 and hosts the local Real Estate Investment Association. Real Estate is his passion. Clint previously worked in drilling fluids and drilling fluids automation for 28 years. He lives in Bayou Blue with his wife and two daughters.

Clint C. Galliano, REALTOR® 985.647.4479 clint.galliano@kw.com Licensed by the Louisiana Real Estate Commission Keller Williams Realty Bayou Partners 985.262.4400 307 Bayou Gardens Blvd Houma, La 70364 Each Office is Independently Owned & Operated

In the realm of wealth building, real estate stands out as a formidable avenue for creating long-term assets and generating passive income. A strategy that has been gaining traction among savvy investors was recently highlighted on the Bigger Pockets real estate podcast, offering a practical approach to real estate investment that eschews the allure of quick gains in favor of a more sustainable, long-term plan.

The 15-Year Mortgage Strategy

The essence of this strategy lies in the acquisition of rental properties financed through 15-year mortgages. The key here is not immediate cash flow but a long-term vision. The initial goal isn’t to secure properties that will rake in substantial profits from the get-go but to find homes that, at the very least, can cover their own expenses through rental income. Ideally, these properties should also allow for a small buffer to be set aside for maintenance and unexpected costs.

Year-by-Year Breakdown:

Year 1: Purchase your first rental property with a 15-year mortgage. Ensure the rent covers the mortgage and expenses, with a little extra for savings.

Year 2 and Onwards: Repeat the process, acquiring an additional property each year under similar financial arrangements.

The Long-Term Payoff

After 15 years, the mortgage on your first property will be fully paid off. This is where the strategy begins to reveal its true potential. The income from this property, no longer siphoned off to pay a mortgage, becomes pure cash flow or can be leveraged through refinancing to extract cash tax-free (note: always consult with a tax professional for personalized advice). This process is then repeated each subsequent year with the next property in line, creating a continuous stream of income.

The Perpetual Money Machine

This approach effectively creates a perpetual money machine. While it does require active management of the properties or the employment of a property manager, the financial rewards can be substantial. It’s a pathway to wealth that, in comparison to traditional career trajectories, offers the possibility of financial independence in a relatively shorter timeframe.

A Sustainable Approach to Wealth

While a 15-year commitment might seem daunting, it’s a blink in the grand scheme of a working life, which often spans 30 to 40 years or more. This real estate investment strategy offers a viable alternative to the traditional retirement plan, potentially allowing for an earlier and more financially secure retirement.

This strategy underscores the importance of patience, planning, and a willingness to look beyond immediate gains for long-term prosperity. Real estate investment, when approached with diligence and foresight, can indeed pave the way to financial freedom and a secure future.

Engage and Learn More

For those intrigued by this wealth-building strategy or seeking further insights into real estate investment, engaging with a knowledgeable professional can be invaluable. Whether through direct communication or following expert-led content, there’s a wealth of knowledge to be tapped into.

Clint C. Galliano, REALTOR® 985.647.4479 clint.galliano@kw.com Licensed by the Louisiana Real Estate Commission Keller Williams Realty Bayou Partners 985.262.4400 307 Bayou Gardens Blvd Houma, La 70364 Each Office is Independently Owned & Operated

Clint C. Galliano, a native of Lafourche Parish, has lived in the Houma-Thibodaux area for over 36 years and is currently a REALTOR® with Keller Williams Realty Bayou Partners in Houma, La. He has been involved with real estate investing since 2017 and hosts the local Real Estate Investment Association. Real Estate is his passion. Clint previously worked in drilling fluids and drilling fluids automation for 28 years. He lives in Bayou Blue with his wife and two daughters.

Congratulation to the agents who made the Top 10 for sales volume at our brokerage!

This is two months in a row that I am in this group. I am deeply honored to be here.

This is an amazing place to work and I really love the family atmosphere of the KW Bayou Partners Brokerage. It is so different than my previous career that I am constantly having to pinch myself to make sure I am not dreaming.

If you are thinking about a career in real estate, let’s talk.

Remember, if you have a real estate need, whether buying or selling, give me a call or shoot me an email. It doesn’t matter if you are outside of my area, I can connect you with a Rockstar Real Estate Agent!

Clint C. Galliano, REALTOR® 985.647.4479

Clint C. Galliano, a native of Lafourche Parish, has lived in the Houma-Thibodaux area for over 36 years and is currently a REALTOR® with Keller Williams Realty Bayou Partners in Houma, La. He has been involved with real estate investing since 2017 and hosts the local Real Estate Investment Association. Real Estate is his passion. Clint previously worked in drilling fluids and drilling fluids automation for 28 years. He lives in Bayou Blue with his wife and two daughters.

Howie Bick is the founder of The Analyst Handbook. The Analyst Handbook is a collection of 16 guides created to help current and aspiring Analysts advance their careers. Prior to founding The Analyst Handbook, Howie was a financial analyst.

Things To Keep In Mind When Starting A Business

Building or creating a business is an endeavor that incorporates a variety of different factors, and touches upon multiple different topics. Within the building of a business, there are lots of ideas to think about, like the amount of capital you may need in order to begin, the type of overhead or expenses you may have on a monthly basis, the type of market or demographic you’ll be catering to, and the type of competition that’s out there. The business landscape is one that requires business owners or managers to manage and handle a variety of tasks and wear multiple different hats at once. Keeping these things in mind, and having a good idea of what’s ahead, will be beneficial for anyone trying to build or create a business.

The Market or Demographic You’re Catering To

Each business or company has a particular demographic or market that they are looking to cater to. The market or demographic a company or business is looking to cater to, is often a group of people who have something in common, like a problem, an issue, or a desire they’re looking to solve. It can be something they need, desire, or want, but the business is looking to provide a solution or deliver the type of results their customers are looking for. Figuring out the market or demographic you’re looking to cater to, is a great place to start. That way, you can get an idea of the types of services they may be looking for, the type of products that may interest them, or the type of solutions they may be looking for. The way a business positions themselves, with their offerings to their customers, plays an important role in the way potential customers view them, and the way they’re viewed within the marketplace.

Competitive Advantages or Competitive Edges

Businesses that are able to carve out a particular niche, or area where they’re successful, often have a competitive edge, or a competitive advantage over the competition. A competitive edge is something that a business does better or more effectively than their competitors, or something that allows them to differentiate themselves within the marketplace. It’s an important element to any company or business, that’s looking to compete in a market where there are lots of options, and many parties looking to fulfill or satisfy their customers desires. Companies can develop competitive advantages through their prior experiences, the type of packages or services they offer to their competitors, or the type of knowledge or information they may have that others don’t. It’s something that’s important to keep in mind, when you’re evaluating whether you may be successful in a certain market, or whether you’re capable of differentiating yourself among the competition.

The Initial or Upfront Costs Associated With Starting

Every business requires a certain amount of investment, or capital in order to begin operating. Whether it’s getting a space and signing a lease, or acquiring the type of machinery you may need to operate, the costs associated with creating or building a business depend on the type of company you’re looking to build, and the types of products or services you plan to offer. It’s important to have a sense of the amount of capital or investment it may cost to create a business. It’s a tough situation when you decide to start a business and invest the capital or resources you do have, to later find out that you don’t have enough, or need to obtain more. By having an idea or a sense of the type of investment a certain business requires you can prepare or plan in advance or prior to creating the business and be better situated to develop or create the business you were looking to build.

The Monthly Costs or Expenditures

Similar to the amount of capital or investment you may need in order to start or build a business, having a sense or an idea of the types of costs or expenses that your business may accrue or cost on a monthly basis is an important metric to keep an eye on. The age-old business equation is revenue minus expenses equals profit. By having an idea of the type of expenses you may accrue, you’re able to get an idea of how much business you need to do, or how much revenue you need to generate in order to make money in a month. You’re also able to have an idea of how much capital or money you need to keep on hand to continue operating and continue running the business. The monthly costs or expenditures associated with a business is an important figure to keep an eye on, and to monitor during the operations of a business, and prior to starting or creating a business.

Personal Expenses Continue to Accrue

Whenever you’re starting something new, a new job, a new company, or a new business, it’s important to keep in mind that your personal expenses continue to accrue. In the beginning stages of building a business, it often takes a bit of time to get going, and to start making the type of money you’re looking to make. That’s why, it’s important to consider that even though you may be starting a new business or a new company, which is great and congratulations, that you’ll still need to find a way to pay bills and provide for yourself. It’s something that’s a bit of a struggle for a new business owner, who’s truly looking to build a business to support themselves, or to generate the type of income they’re looking for. Preparing and planning in advance is something that can be very beneficial to lightening the load and making the transition an easier process or ordeal for you financially.

Conclusion

Building a business is something that comes with lots of different ideas to keep in mind and brings in to play lots of different factors as well. The market or demographic you’re trying to cater to, is an important part of any business, as it’s the group of people or companies you’re looking to interact with and find a way to provide value to. The competitive edge or competitive advantage a company has, is important in a company’s efforts to stand out within a marketplace or find a way to differentiate itself among its competitors. By having a sense of how much capital or investment you might need to start a business, you can have an idea of whether you have enough to begin, or whether you need to wait longer, or figure out another way. Having that sense of how much investment it might require, can save you spending lots of your money on something that may not be feasible just yet, or a bit out of reach. The monthly costs or expenditures that a business requires, is important to know how much revenue you need to generate, and the type of capital or money you need to keep on hand in order to continue operating. A lot of what corporate finance is, is managing the finances behind a business, making sure that the business has what it needs to continue operating, and finding ways to continue to grow and develop the business as well. Even though you may be starting something new, and you need time to bring it into fruition, personal expenses are something that continue to accrue, and are important to keep in mind when building a business. All in all, creating a business is something that comes with lots of different factors, a lot more than the few we were able to highlight. We hoped this helped and shined light on some of the important factors to consider when starting or creating a business.

And, as always, let me know what you think in the comments. Ask questions, tell your story.

If you like my articles, please share them with others and subscribe to this blog.

In the span of these last five months I have had two meetings with my manager(s) and HR to let me know that due to market conditions, among other thing things, my position was being eliminated.

The first conversation was a choice between an early retirement package or working in another state. The second gave no options.

This is how I joined the ranks of the recently unemployed. It may or may not differ from yours, but that is not the point. I will lay out some guidelines to point you in the right direction, especially if you are feeling overwhelmed and not sure what to do.

What next?

“What next?” is the question you may be asking yourself. The first thing you should do is understand that this situation is not a reflection on you. This is not an indication of your self-worth. Especially at this time, thousands of people are being laid off.

Take a breather, relax, or, if possible, a mini-vacation. Let your mind recuperate from the stress.

Stay the Course or Change Direction?

The next step is to decide if you want to continue doing what you have been doing. Some of you have knowledge, skills, and talents that easily transfer to other industries while others may need to adapt their skills to new areas.

If needed, don’t be afraid to train for something new. We will discuss training in more detail below.

The point is, from my perspective, the oil and gas industry will not be booming soon, so don’t wait around for it to pick back up.

How Much Do I REALLY Need to Spend?

At this point, it is a good idea to review your finances. If you have not done so already, put together a personal balance sheet. This totals all of your assets and all of your liabilities. This will help you to visualize what resources you have and what debt you owe.

Then tally up all of your expenses. Look at this long and hard to decide what is essential and what can be cut or reduced. Examples can be premium movie channels, cable TV, any type of subscription that is not essential.

File for unemployment benefits if you are able. The weekly payment amount varies from state to state and also depending on other factors like recent salary. In my case, I am eligible for $247 per week in unemployment benefits.

There should also be an additional federal benefit of $600 per week on top of the state benefit due to the pandemic. Your state employment website should allow you to indicate that the pandemic was partially or wholly the cause for your being released.

Now What?

At this point, you should have a thorough understanding of where you are financially, what assets you have, what bills you owe, and a good idea on whether or not you will continue doing what you were doing or establish a career in a new industry.

If you are an IT Professional, it’s easy to transfer your capabilities to a different industry because the requirements are relatively similar, no matter what industry.

If your career was more specialized, say Drilling Fluids Technical Professional, that job description won’t show up in other industries.

Start to look at training opportunities for your new career choice. Your state employment website should have a section on training to prepare you for a different job. Pretty much every major job search engine provides you with a list of free training resources. Use them. Take advantage of the opportunity to add to your skill set.

You will get through this. You have the choice to be better for this. Seize control and be the best you can be!

Remember, if you have a real estate need, whether buying or selling, give me a call or shoot me an email. It doesn’t matter if you are outside of my area, I can connect you with a Rockstar Real Estate Agent!

Clint C. Galliano, REALTOR® 985.647.4479

And, as always, let me know what you think in the comments. Ask questions, tell your story. If you like my posts, please share them with others and subscribe to this blog.

The oil and gas industry is in turmoil and service companies, in particular, are reducing their footprint in an attempt to weather the double-pronged attack of oil price wars and pandemic lockdowns.

Until yesterday, I worked for one of those companies, as some of you long-time readers may know.

I received a phone call from my manager, and HR, telling me that due to the current environment, my position was being eliminated.

It is not a bad thing. I only took the position back in January because I was unsure of what I wanted to do when my regional position was eliminated. I figured that they went through a lot of effort to keep me in the company and I didn’t have an immediate alternative plan, so I worked the job in Houston.

Then the pandemic hit and everyone was on lockdown. Luckily, I was able to continue working, from home.

BUT, during this time, I realized that I did not want to go back to Houston for work. We decided that I would continue working, as long as I could do it from home, and as soon as I was told that I needed to show up in Houston, I would resign.

It seems things have worked out for the best, because instead of just resigning, I am leaving with an early retirement severance package!

Because of this, I am now free to explore other opportunities…One will be to continue to be involved in real estate, but to a larger degree. I will continue to invest, but now I am pursuing a realtor’s license.

I will also be available to consult on any innovation projects that might come my way. This will allow me to flex my mental muscle “coming up with cool shit” as a colleague is fond of saying.

I will also look for small businesses that the owners are preparing to retire with no one to take them over. I will only pursue them if they are profitable. It should be easy to make a good deal on something like that when the options are sell at a discount or shut it down.

Merry Christmas! Happy Holidays! Happy Solstice! Happy Hanukkah! Joyous Kwanzaa! Yuletide Greetings! Joyeux Noël! Feliz Navidad! Season’s Greetings! Happy New Year! Joy! Celebrate! Be Merry! And most of all, wishing all of you who read this a new year full of peace and joy!

I’m sitting here between Christmas and New Year’s Day contemplating the future. To paraphrase Game of Thrones, “Change is Coming”.

As many of you know, we decided to start investing in real estate as a buffer to the ups and downs of my chosen industry, Oil and Gas Exploration. I was able to make it through some of those ups and downs in the past, maybe by luck, or because what I was working on was important. At one point, I did take a demotion and worked in the field (offshore, on the rigs, for about a year, but was able to move out of that role and on to greater things.

Which brings us to current times. Things have dipped again.

I usually take the last two to three weeks of the year off since I usually don’t use all of my vacation throughout the year. I was sitting at home and my supervisor called and asked if I was at the office. Since I wasn’t, he asked if I could come in. This told me that something was up because his office is over 100 miles away and if he is at my office, then it must be my turn.

And it was, but with a twist. I was offered a choice between an early retirement package or a rotational position working in Houston.

My darling wife and I contemplated the choices for a couple of days. Ultimately, we decided that it would be best to take the position in Houston. While we would be OK with me not working for a while, ultimately, it was our need of medical insurance that swayed our decision. Speaking of medical insurance, my next article will cover my experience in trying to get a quote for it and the fraud potential inherent in the Louisiana Medicaid Program.

Working a rotational job in Houston would mean finding a place to stay when working and time away from the family, but it also would mean that for two weeks out of every four, I would be off of work and free to do as I please.

This should allow for catching up on projects around the house and more opportunity to generate passive income.

The down side is that I will not be in town for some of the Bayou Real Estate Investor Networking meetings. I will continue to organize them, but will have to rely on other members to host when I cannot attend.

Additionally, if any of you live in or around North Houston / Humble / Kingwood and know of decent rentals at a good price, please contact me!

And, as always, let me know what you think in the comments. Ask questions, tell your story.

If you like my posts, please share them with others and subscribe to this blog.

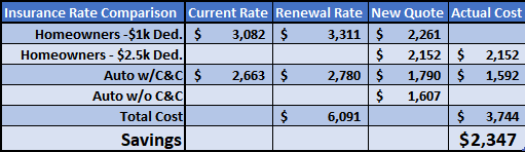

Actual Numbers. Blanks are where numbers were not needed.

Today’s topic is about reviewing your insurance coverages and ensuring that you are properly covered at the best rate. It also touches on customer service and some things that caused me to look for a change.

Isn’t it crazy that it is December already? The end of the year, the end of the decade. Here at the Galliano household we are busy buying Christmas gifts for the family and coordinating our schedules for band concerts, choir concerts, and a birthday.

It is also about paying year-end bills…we have property taxes on our rentals, but that is covered easily by the rent. We also have property taxes on our residence and another property. We can’t do a whole lot about what we are paying on those taxes.

Then there is insurance. Since we paid off our mortgage years ago, we have to purchase homeowners’ insurance outright. AND, since we originally moved into our house right before Christmas, our insurance comes due at Christmas time.

On top of that, our auto insurance is due on 02-Jan-2019. So that totals up to a lot of bills at the end of the year.

The current (as of this writing) agency we use has been providing me with insurance for around 20 years. But I am not happy with them. Over the last four to five years, my “agent of record” has changed at least four times. And the only way I find out about it is if I call with a question. On top of that, when the renewal notices came in this year, they totaled to a little over $6000! I asked for a quote at a lower home value, because the company we are covered with has an auto-escalate policy and increases the coverage value every year, thus increasing the premium. The renewal value was for $291,000. My home is probably worth about $250,000 on a good day.

I also asked for an increased deductible, increasing the deductible from $1000 to $5000. They couldn’t do that. They could only do two percent. So I asked the agent to quote me for coverage on a more accurate home value. Two to three days later, I get a quote for a home value of $232,000. Yes, it was $1000 or so cheaper than the renewal quote, but it was not for the home value that I requested. Because of this, my search for a new provider began.

One of my fraternity brothers offered to give us quotes. In going through that process, we were able to get the coverage we wanted at much lower rates. Between the home and auto coverage, it only cost us $3,744, for a savings of $2,347 between the two. That is almost $200 per month of savings! That will cover a trip to Disneyworld for Mardi Gras! LOL

Tips for Insurance

Below are some tips for getting the most for the least when dealing with insurance:

Review your policies annually to ensure accurate coverage – Make sure you aren’t paying for a home value above the replacement cost of your home

Try to pay your policy in a lump sum – Some providers will give you a discount for paying in full

It pays to shop prices every once in a while

Ensure you have a good relationship with your agent – Find an agency that provides you with a single point of contact and will notify you of any changes

Your home value is not your home replacement value

Depending on the age of your vehicle, you may not need comprehensive and collision insurance

Be in a financial position to be able to pay your policies lump sum

And, as always, let me know what you think in the comments. Ask questions, tell your story.

If you like my articles, please share them with others and subscribe to this site.