In the realm of wealth building, real estate stands out as a formidable avenue for creating long-term assets and generating passive income. A strategy that has been gaining traction among savvy investors was recently highlighted on the Bigger Pockets real estate podcast, offering a practical approach to real estate investment that eschews the allure of quick gains in favor of a more sustainable, long-term plan.

The 15-Year Mortgage Strategy

The essence of this strategy lies in the acquisition of rental properties financed through 15-year mortgages. The key here is not immediate cash flow but a long-term vision. The initial goal isn’t to secure properties that will rake in substantial profits from the get-go but to find homes that, at the very least, can cover their own expenses through rental income. Ideally, these properties should also allow for a small buffer to be set aside for maintenance and unexpected costs.

Year-by-Year Breakdown:

Year 1: Purchase your first rental property with a 15-year mortgage. Ensure the rent covers the mortgage and expenses, with a little extra for savings.

Year 2 and Onwards: Repeat the process, acquiring an additional property each year under similar financial arrangements.

The Long-Term Payoff

After 15 years, the mortgage on your first property will be fully paid off. This is where the strategy begins to reveal its true potential. The income from this property, no longer siphoned off to pay a mortgage, becomes pure cash flow or can be leveraged through refinancing to extract cash tax-free (note: always consult with a tax professional for personalized advice). This process is then repeated each subsequent year with the next property in line, creating a continuous stream of income.

The Perpetual Money Machine

This approach effectively creates a perpetual money machine. While it does require active management of the properties or the employment of a property manager, the financial rewards can be substantial. It’s a pathway to wealth that, in comparison to traditional career trajectories, offers the possibility of financial independence in a relatively shorter timeframe.

A Sustainable Approach to Wealth

While a 15-year commitment might seem daunting, it’s a blink in the grand scheme of a working life, which often spans 30 to 40 years or more. This real estate investment strategy offers a viable alternative to the traditional retirement plan, potentially allowing for an earlier and more financially secure retirement.

This strategy underscores the importance of patience, planning, and a willingness to look beyond immediate gains for long-term prosperity. Real estate investment, when approached with diligence and foresight, can indeed pave the way to financial freedom and a secure future.

Engage and Learn More

For those intrigued by this wealth-building strategy or seeking further insights into real estate investment, engaging with a knowledgeable professional can be invaluable. Whether through direct communication or following expert-led content, there’s a wealth of knowledge to be tapped into.

Clint C. Galliano, REALTOR® 985.647.4479 clint.galliano@kw.com Licensed by the Louisiana Real Estate Commission Keller Williams Realty Bayou Partners 985.262.4400 307 Bayou Gardens Blvd Houma, La 70364 Each Office is Independently Owned & Operated

Clint C. Galliano, a native of Lafourche Parish, has lived in the Houma-Thibodaux area for over 36 years and is currently a REALTOR® with Keller Williams Realty Bayou Partners in Houma, La. He has been involved with real estate investing since 2017 and hosts the local Real Estate Investment Association. Real Estate is his passion. Clint previously worked in drilling fluids and drilling fluids automation for 28 years. He lives in Bayou Blue with his wife and two daughters.

Wow…It has been a while since I have posted an article here! I’ve been a bit busy with life and being a Real Estate Agent.

I just wanted share an update on how my real estate sales business did this year.

This was my first full year as a real estate agent, so it has allowed me to look over my numbers and performance to establish a baseline to grow from. Here are the highlights.

In the past year, I added 398 contacts to my database. What is the big deal about that? For every fifty people that you market to at least 12 times a year, you can expect one sale. So that allowed me to add four potential additional sales a year going forward.

Out of those contacts, 275 were potential buyers or sellers. That lead to a total of 87 sales opportunities, with 24 being listing opportunities and 63 being buyer opportunities.

I closed 16 total units with a production volume of $2,464,390. That was 7 listings at $880,500 and 9 buyer sales at $1,583,890. The average sale amount was $154,024.

I ended the year with 5 pending deals carried into 2022. 4 listings and 1 buyer. As of today, 17-Jan-2022, one of those listings has closed and buyer sale should close this week.

Remember, if you have a real estate need, whether buying or selling, give me a call or shoot me an email. It doesn’t matter if you are outside of my area, I can connect you with a Rockstar Real Estate Agent!

Now for the business breakdown…I had a Gross Revenue of $81,468. This included $68,581 of Gross Commission Income, $9,574 in referral Commission, and $3,308 of sales of oilfield testing equipment liquidated for a client.

Out of that, I paid $20,502 in “Company Dollar”, (split of my commission to the brokerage), $4,115 in Royalties to Keller Williams Realty International, $1,624 COGS, (client split of testing equipment sales), and $9,397 in operating expenses. OPEX includes advertising, training, dues, professional fees, etc.

Overall, I had a Gross Profit of $37,720 before taxes.

Not a bad start for my first full year! AND, this was while also serving as the Market Center Tech Trainer, in addition to the whole area shutting down for the whole month of September due to Hurricane Ida.

If you are interested in becoming a real estate agent, get in touch with me. It’s a really cool career and much more enjoyable than my previous career.

And, as always, let me know what you think in the comments. Ask questions, tell your story.

If you like my posts, please share them with others and subscribe to this blog.

Clint C. Galliano, a native of Lafourche Parish, has lived in the Houma-Thibodaux area for over 36 years and is currently a REALTOR® with Keller Williams Realty Bayou Partners in Houma, La. He has been involved with real estate investing since 2017 and hosts the local Real Estate Investment Association. Real Estate is his passion. Clint previously worked in drilling fluids and drilling fluids automation for 28 years. He lives in Bayou Blue with his wife and two daughters.

Howie Bick is the founder of The Analyst Handbook. The Analyst Handbook is a collection of 16 guides created to help current and aspiring Analysts advance their careers. Prior to founding The Analyst Handbook, Howie was a financial analyst.

Things To Keep In Mind When Starting A Business

Building or creating a business is an endeavor that incorporates a variety of different factors, and touches upon multiple different topics. Within the building of a business, there are lots of ideas to think about, like the amount of capital you may need in order to begin, the type of overhead or expenses you may have on a monthly basis, the type of market or demographic you’ll be catering to, and the type of competition that’s out there. The business landscape is one that requires business owners or managers to manage and handle a variety of tasks and wear multiple different hats at once. Keeping these things in mind, and having a good idea of what’s ahead, will be beneficial for anyone trying to build or create a business.

The Market or Demographic You’re Catering To

Each business or company has a particular demographic or market that they are looking to cater to. The market or demographic a company or business is looking to cater to, is often a group of people who have something in common, like a problem, an issue, or a desire they’re looking to solve. It can be something they need, desire, or want, but the business is looking to provide a solution or deliver the type of results their customers are looking for. Figuring out the market or demographic you’re looking to cater to, is a great place to start. That way, you can get an idea of the types of services they may be looking for, the type of products that may interest them, or the type of solutions they may be looking for. The way a business positions themselves, with their offerings to their customers, plays an important role in the way potential customers view them, and the way they’re viewed within the marketplace.

Competitive Advantages or Competitive Edges

Businesses that are able to carve out a particular niche, or area where they’re successful, often have a competitive edge, or a competitive advantage over the competition. A competitive edge is something that a business does better or more effectively than their competitors, or something that allows them to differentiate themselves within the marketplace. It’s an important element to any company or business, that’s looking to compete in a market where there are lots of options, and many parties looking to fulfill or satisfy their customers desires. Companies can develop competitive advantages through their prior experiences, the type of packages or services they offer to their competitors, or the type of knowledge or information they may have that others don’t. It’s something that’s important to keep in mind, when you’re evaluating whether you may be successful in a certain market, or whether you’re capable of differentiating yourself among the competition.

The Initial or Upfront Costs Associated With Starting

Every business requires a certain amount of investment, or capital in order to begin operating. Whether it’s getting a space and signing a lease, or acquiring the type of machinery you may need to operate, the costs associated with creating or building a business depend on the type of company you’re looking to build, and the types of products or services you plan to offer. It’s important to have a sense of the amount of capital or investment it may cost to create a business. It’s a tough situation when you decide to start a business and invest the capital or resources you do have, to later find out that you don’t have enough, or need to obtain more. By having an idea or a sense of the type of investment a certain business requires you can prepare or plan in advance or prior to creating the business and be better situated to develop or create the business you were looking to build.

The Monthly Costs or Expenditures

Similar to the amount of capital or investment you may need in order to start or build a business, having a sense or an idea of the types of costs or expenses that your business may accrue or cost on a monthly basis is an important metric to keep an eye on. The age-old business equation is revenue minus expenses equals profit. By having an idea of the type of expenses you may accrue, you’re able to get an idea of how much business you need to do, or how much revenue you need to generate in order to make money in a month. You’re also able to have an idea of how much capital or money you need to keep on hand to continue operating and continue running the business. The monthly costs or expenditures associated with a business is an important figure to keep an eye on, and to monitor during the operations of a business, and prior to starting or creating a business.

Personal Expenses Continue to Accrue

Whenever you’re starting something new, a new job, a new company, or a new business, it’s important to keep in mind that your personal expenses continue to accrue. In the beginning stages of building a business, it often takes a bit of time to get going, and to start making the type of money you’re looking to make. That’s why, it’s important to consider that even though you may be starting a new business or a new company, which is great and congratulations, that you’ll still need to find a way to pay bills and provide for yourself. It’s something that’s a bit of a struggle for a new business owner, who’s truly looking to build a business to support themselves, or to generate the type of income they’re looking for. Preparing and planning in advance is something that can be very beneficial to lightening the load and making the transition an easier process or ordeal for you financially.

Conclusion

Building a business is something that comes with lots of different ideas to keep in mind and brings in to play lots of different factors as well. The market or demographic you’re trying to cater to, is an important part of any business, as it’s the group of people or companies you’re looking to interact with and find a way to provide value to. The competitive edge or competitive advantage a company has, is important in a company’s efforts to stand out within a marketplace or find a way to differentiate itself among its competitors. By having a sense of how much capital or investment you might need to start a business, you can have an idea of whether you have enough to begin, or whether you need to wait longer, or figure out another way. Having that sense of how much investment it might require, can save you spending lots of your money on something that may not be feasible just yet, or a bit out of reach. The monthly costs or expenditures that a business requires, is important to know how much revenue you need to generate, and the type of capital or money you need to keep on hand in order to continue operating. A lot of what corporate finance is, is managing the finances behind a business, making sure that the business has what it needs to continue operating, and finding ways to continue to grow and develop the business as well. Even though you may be starting something new, and you need time to bring it into fruition, personal expenses are something that continue to accrue, and are important to keep in mind when building a business. All in all, creating a business is something that comes with lots of different factors, a lot more than the few we were able to highlight. We hoped this helped and shined light on some of the important factors to consider when starting or creating a business.

And, as always, let me know what you think in the comments. Ask questions, tell your story.

If you like my articles, please share them with others and subscribe to this blog.

I hope everyone is doing well. I am learning the ins and outs of being a REALTOR®. The kids are preparing to go back to school with a staggered schedule and a blend of virtual and in-person learning. AND, no extracurricular activities such as marching band, various band and choir competitions, etc.

This will be far different from what they are used to. They hesitant about their ability to do school work consistently outside of a classroom environment. We will have to help them to develop new habits to successfully reach their goals. Which brings us to our topic: Habits and How to Change Them.

Habits & Productivity

I recognized that habits are responsible for productivity at a young age. I grew up with undiagnosed ADHD and had trouble focusing on any given task. I would generally get bored and move on to something more exciting.

My maternal grandfather, whom I am named after, recognized this and pulled me aside to tell me a story one day. He told me of Bethlehem Steel and how they worked and worked, but just couldn’t seem to make progress. After continued diminishing profits and increased backlogs, the CEO brought in a consultant to tell him what the problem was. The consultant studied the company’s business and reported back to the CEO. His findings were that across the company, tasks were started, then paused, to jump to other tasks. This happened over and over again, delaying production.

His recommendation was to prioritize the tasks needing to be accomplished, with the most important task at the top of the list. But the biggest change was that they could not move on to another task until the current task was completed.

This practice was implemented and Bethlehem Steel went on to become the second largest steel company in the US.

This story had a big impact on me in that it drove me to develop the habit to focus on a task until either it was completed or nothing more could be done with it.

In researching the details of the Bethlehem Steel story, I discovered some interesting things. This happened over 100 years ago, (1918), Charles Schwab was the CEO, and the practice that turned things around is called “The Ivy Lee Method”. While Mr. Schwab may sound familiar, the ILM did not, but I recognized it as the basis for a lot of time management programs. Making a prioritized list is now a common approach for productivity.

The ILM requires that at the end of each day, you make a list of the six most important tasks that need to be accomplished the next day. Then you complete the first item before moving on to the next item. Any leftover items on the list move to the next day’s list.

This method is lauded as being simple to follow, so that makes it effective when practiced. But sometimes, having too many “To Dos” becomes daunting. It can become an impenetrable wall discouraging you from doing more.

Gary Keller ran across this when he was building Keller Williams Realty. What he realized, is that your list should only be comprised of one thing, as described in his book, The One Thing. That method involves doing the one thing that makes everything else in your day easier/better/more productive.

Knowing vs. Doing

Based on the ILM, The One Thing, and various models, it seems we have many models to follow to accomplish our daily goals. We know what needs to be done. Or at least can easily find out/figure out those things.

Some people find the real struggle is actually doing them. I find that it all boils down to what you are willing to do to achieve your goals. Excuses get made as to why you aren’t, can’t, or won’t do something. But they are just that: EXCUSES.

Here is something else that stuck with me from when I was younger: a Stephen King short story called “Survivor Type”. The story is a bit disturbing and somewhat gory, as Stephen King stories are want to be.

Synopsys: A doctor is stuck on an atoll after some bad decisions that ruined his life. He is determined to live. He then proceeds to do disturbing things to survive.

When I read this story, the question that kept running through my mind was “What would you be willing to do to accomplish your goals?” To me, that is the take-away.

If you are in the habit of staying in your comfort zone and your focus changes like a leaf blowing in the wind, it will be hard to accomplish your goals.

Habits

The first step is to have a goal.

Then have a heart- to- heart with yourself to determine what you are willing to do to achieve your goal.

Start practicing a model that will help you reach your goal. Do it daily.

Eventually, the practice of the model will become a habit. This is how you succeed.

And, as always, let me know what you think in the comments. Ask questions, tell your story.

If you like my posts, please share them with others and subscribe to this blog.

We are still doing fine and have been able to go back to the gym, so that is a nice expansion on our workout routine from the lockdown.

I have completed my 90 Hour Real Estate Salesperson training course and will be taking the national and state exams this week. #WishMeLuck

Today I wanted to talk about outsourcing. As a real estate investor focused on expanding, you continuously search for properties. There are numerous ways to accomplish that on your own, whether it is “Driving for Dollars”, (drive around looking for vacant properties), searching the MLS, tax sales, or any of the other numerous ways to find properties.

There is an issue with all of these methodologies in that if you are doing them, what aren’t you doing to work on your business?

So, why not outsource your search for properties?

Put in a little effort to document your criteria in a Property Search One Sheet and share it with anyone and everyone. This allows other people to identify properties that meet your criteria and bring them to you, thereby increasing the input into your funnel.

The people you share it with can be family, friends, acquaintances, and even property wholesalers.

The oil and gas industry is in turmoil and service companies, in particular, are reducing their footprint in an attempt to weather the double-pronged attack of oil price wars and pandemic lockdowns.

Until yesterday, I worked for one of those companies, as some of you long-time readers may know.

I received a phone call from my manager, and HR, telling me that due to the current environment, my position was being eliminated.

It is not a bad thing. I only took the position back in January because I was unsure of what I wanted to do when my regional position was eliminated. I figured that they went through a lot of effort to keep me in the company and I didn’t have an immediate alternative plan, so I worked the job in Houston.

Then the pandemic hit and everyone was on lockdown. Luckily, I was able to continue working, from home.

BUT, during this time, I realized that I did not want to go back to Houston for work. We decided that I would continue working, as long as I could do it from home, and as soon as I was told that I needed to show up in Houston, I would resign.

It seems things have worked out for the best, because instead of just resigning, I am leaving with an early retirement severance package!

Because of this, I am now free to explore other opportunities…One will be to continue to be involved in real estate, but to a larger degree. I will continue to invest, but now I am pursuing a realtor’s license.

I will also be available to consult on any innovation projects that might come my way. This will allow me to flex my mental muscle “coming up with cool shit” as a colleague is fond of saying.

I will also look for small businesses that the owners are preparing to retire with no one to take them over. I will only pursue them if they are profitable. It should be easy to make a good deal on something like that when the options are sell at a discount or shut it down.

How are you doing? How are you handling the mis-named “social distancing”? We are going a bit stir-crazy. I am probably more used to the isolation and not being able to go anywhere from when I worked offshore in the oil and gas industry. This is a lot nicer than sitting on a floating rig that you have to fly for one to two hours in a helicopter to reach.

Feel free to reach out if you need to talk to someone. It actually helps with the isolation.

Now, on to the content…

Due to the statewide Stay at Home order here in Louisiana, our local REIA are not able to get together for our monthly meeting. So, I’ve decided to move it online, replacing it with a livestream. Since it covered topics that I think are relevant to a larger audience, I’ve decided to share it with this community, too.

In this video, Tim Blanchard, of Allegiance Home Lending, discusses how mortgage rates work, what the impact is from the Q1 2020 FED Interest Rates on mortgages and regular loans, and gives advice on utilizing SBA Coronavirus relief options.

Things you will learn in this video:

What affects mortgage rates.

What mortgage rates are based on.

What drives a change in mortgage rates.

How Lenders’ Credit Score Criteria have changed in this environment.

SBA Coronavirus relief opportunities for businesses.

Today, we are going to continue where the last article left off. We are going to go over the lessons learned from my experience buying a business with partners. I will list them out with short descriptions. There is no particular order to the list. Any names mentioned other than my own have been changed to protect the innocent…

Lessons

Learned

Partners (The Team) –Our team consisted of four partners. Bob and Carl are the majority investors and took out an SBA loan to acquire the business. John and I are minority partners and not party to the SBA loan. Because Carl, John, and I all have full-time jobs and at the time Bob did not, the plan was that Bob would learn and operate the business until we could afford to put someone else running the business, leaving Bob to pursue his personal interests. See my last article for how that all turned out.

Recommendations:

Be transparent about

individual drivers. Becoming your own boss and becoming wealthy eventually

become competing interests for an entrepreneur.

Professional respect

is critical. Tolerance is listening to every idea quietly. Professional respect

is availability, transparency, punctuality, and preparedness.

Autonomy must be

earned, never assumed in a partnership.

Bad habits are hard

to break in others.

Operating Agreement/Bylaws – Depending on whether you have a Limited Liability Company (LLC) or a Corporation (Co), you should have either an operating agreement or bylaws to govern how the business will be run. In our case, since we had a corporation, we had bylaws. We deliberated on what to include in these bylaws to ensure smooth operations, but did not go far enough. They did not spell out the duties of each partner & role, because we thought that all of us being adults, we would do what was needed to be successful. What we realized was that we each viewed the word through a very personalized lens and what seems obvious to one, (or two, or even three), is not obvious to everyone and if the fourth person feels strongly enough about it, they just will not go along unless forced to. And even then, although begrudgingly agreeing in discussion, they will still fight and obstruct the wishes and decisions of the group. If we had, as a group, decided on the duties for each role and assigned responsibilities for each role to each member of the group, then documented it in the bylaws, it would have made things a lot clearer.

Recommendations:

The operating agreement or bylaws should also include a

defined exit strategy that everyone has agreed to and is committed to

following. It should have defined triggers that initiate the exit strategy.

These triggers should be something that the partners can easily monitor and

measure against.

It should also be spelled out how to handle decisions and

requests. In our case, decisions initially required unanimous board approval.

We amended the bylaws later to only require a two-thirds majority due to the

one partner asking for a solution to a problem, but not liking the board

recommendations, then never implementing the solutions.

Due Diligence – Nowhere near enough due diligence was done on this business or partners. We did not understand enough about how either operated. The revenue the company was making included the previous owner doing work on weekend “off-book” to get jobs out & keep expenses down. It also relied heavily on promotion via owner visits with distributors and their personal relationship. We had no relationships.

Additionally, having a partner who tells the group he agrees

with the intention of not taking any profits for three years, but assigns

himself a $100,000 per year salary and in the first week of operation directly

violates the ground rules we set up for operating the business. We, (the other

three partners), realized that the fourth partner had pursued the investment

deal to set himself up with a kingdom where he was king. #AvoidDat

Recommendations:

Know how the business operates prior to purchase.

Calculate how much revenue you need to make to break even.

Have a budget that takes into account ALL costs to operate.

Unless you are laundering money for drug cartels, whatever

starting capital you have isn’t enough.

That much isn’t enough, either.

Planning to grow? Triple the previous statement.

Financials –While we started out with modest working capital, we had no understanding of our run rate, break-even point, or runway length. In other words, we did not know how much it cost us to operate, how much we needed to make to break even, or how long we could operate with the amount of working capital we had. We eventually figured those things out, but not until it was too late. Also, another point to make, as referenced in a previous article, you have to pay attention to Cash Flow to stay on top of your business finances. We utilized the accrual method of accounting, but did not regularly look at the cash flow reports. Because of this, we would account for interest paid on our loan from the Income Statement (P & L), but did not account for principle repayment in any of our break-even or forecasting exercises until almost two years into the business.

Recommendations:

The person managing the business needs to have a fundamental

understanding of basic accounting and business / financial principals. This is

a KEY point and will lead to many headaches if not followed.

Know your costs to operate, to the penny! AND, make sure you

include labor!

Cash is King! When you run out of working capital, that is

pretty much the end of the business.

Gross margins should be higher than thirty percent. If not,

this will lead to a death spiral for the company.

Sales – The business we purchased operates, (soon to be preterite or past-tense?), conducted sales via a convoluted structure. The products are sold via distributors to building supply centers for builders. So if an end user wants to use our product, they get their builder to point them to their preferred building supply store, where they can look at brochures or in some instances, floor models to decide on what they would like. They then request a quote. That request comes to our operation, is processed, and returned to the building supply store salesperson. That salesperson has limited information on the product nor incentive to sell it.

From our end, we pay a commission to a sales agent to

promote our products to the distributors, who in turn make them available in

building supply stores. This is too far removed from the end buyers and in my

opinion, not an effective spend.

Recommendations:

Agencies DO NOT replace effective sales people! Agencies

represent a large portfolio of products and do not focus on pushing your

product(s) 24/7.

It doesn’t matter what your product is if you and your team

cannot sell the product(s). No sales = No revenue = No profit = bankrupt

company.

It does not matter how much you cut costs or control

spending if you and your team cannot sell the product(s). (See equation above)

Operations / Efficiency – Prior to closing the deal on the business, since Bob was going ot be operating it, we requested that Bob create a budget and document processes for what the business would need to run. He never gave us a budget, nor processes, even after being in the business for a couple of years. His initial excuse was that he had to be working IN the business to understand how the business operated (for processes) and that we, as the board, should be giving him a budget that he could spend. These were two more missed #RedFlags in our journey that should have told us to run, not walk, to the nearest exit. As of today, there are still no documented processes. We kind of have an idea what our budget is through reviewing financials, but we don’t trust the numbers because they are constantly being adjusted. So, we only have an idea, and nothing from Bob. Ultimately, there are still a lot of inefficiencies in the way the business is being run.

Recommendations:

Inefficiency is

expensive and cripples or kills a company. From the start, focus on efficiency

of process, capital, communication, and decision-making.

Be deliberate and

realistic about growth rate. In projections and practice. Year over year

revenue and product volume increases have to be realistic and managed to avoid unmet

expectations and quality issues. It’s nice to have targets, but remember that

you need sales to support targets (see Sales section below). And it is much

easier to have a customer wait for quality than to apologize for a sparkly

piece of crap.

Product Management –This business has about eight main products with practically infinite levels of customization, not counting special-order material types. Every order is a custom order with many options to choose from. There are forty-five different options to choose from when requesting a quote. This leads to decision fatigue and indecision in customers. Ultimately, our quote/win ratio was very low. We suspect that most customers that requested a quote had already decided on something else by the time they received the quote back. Additionally, “Bob” was continuously wanting to add new products to the portfolio because they were the latest hot thing selling.

Recommendations:

Have IP, a unique desirable product, or both. If you have

neither, shoot it in the head, kill the deal, pull the plug, or whatever

euphemism you want to think in. Unless your goal is to be your own boss, then

feel free to limp along for eternity (or until your cash runs out).

Keep or reduce your product line to your top sellers. Based on the Pareto Principle, roughly 80% of your business should come from your top 20% of sales. (Just a note, it will not be exact. This is a rough guideline) So, find out what products make up the majority of your revenue if you already have a large portfolio of products and focus on selling those products. If you only have a few products, keep this idea in mind before adding new products. Which leads to the next one…

Before adding a new product to the portfolio, always write

up a business case and do sales/cost impact projections. In fact, this should

also be done for any request or change to a product or portfolio.

Product customization is less important that total customer

buying experience. If you make it easy for your customer to buy your product,

you will have more sales.

22-Nov-2019

As of right now, the business is still operating. I do not

know how much longer that will be the case. It continues to limp along, hanging

by a thread.

Stay tuned for further updates…

And, as always, let me know what you think in the comments. Ask questions, tell your story.

If you like my posts, please share them with others and

subscribe to this blog.

Wow, it has been a while since I’ve written anything here.

Things have been busy, to say the least, between my regular job and family. My

oldest started high school marching band as a freshman and her schedule is

brutal! (Translation: Lots of after-school practice, football games, and

marching competitions).

Today we are going to talk about when things don’t go right

in a business, from a finance perspective based on a business I am involved in.

The names have been changed to protect the innocent.

Business History

In March of 2017, a group of former colleagues, with me as a

minor investor, purchased a door manufacturing business. At this point, none of

us had ever been involved in that industry, but we thought that between the

four of us, we could figure everything out and grow the business.

Prior to the purchase, we examined the prior owner’s books

and he seemed to be making decent revenue and profit. We tried to analyze Cost

of Goods Sold (COGS) and Expenses to get a good handle on what our potential

revenue could be.

Because three of us were working full time jobs, the fourth partner, we’ll call him Bob, was going to run the business initially, until we could grow the business enough to hire someone to manage it.

We attempted to get Bob to put together a pro forma operating expense projection, but he kept claiming “he would not be able to accomplish this until he was actually working IN the business and understood everything”. RED FLAG #1 (In hindsight, this should have shut down the deal for us.)

Once we purchased the business, Bob assigned himself a $100,000 per year salary because that was what he “needed” to survive on. We, the other investors, had not begun to understand the business’s key financial benchmarks at this point, so let it slide. RED FLAG #2

After six months or so of this, we begin to realize that our working capital was steadily draining. In addition to Bob arguing against every suggestion the board, (other three investors), would make to improve things, agreeing to implement the suggestions, then never acting on them. We slowly started to realize that even though we all agreed at our initial gathering that this was an investment to grow and either sell it for a profit or, after three years of profit reinvestment, provide cash flow and dividends, Bob was acting as if he was setting up Bob’s Kingdom. He wanted to run the business exactly as the previous owner had run things. RED FLAG #3

We made changes. First, we reduced the salary to $50,000, a

figure more in line with the position. Then we removed him as President. We

attempted to replace him with a salesman we brought on and moved Bob into the

sales role, but since Bob was still involved and also trained the salesman, he

was set up to fail. Bob did not teach him everything and did not say anything

when things slipped through the cracks until after we noticed a couple of

months down the line.

Current Status

The business continues to limp along. We have not put any

more capital into it. Bob occasionally takes out small invoice-secured loans

when the bank account gets too low. He is working at another job and has the

lead employee mostly running the business.

We other investors have mostly given up on expending more

than just a nominal effort to expand the business since no advice given is

followed. We came up with plans and strategies on how to streamline the

business and improve revenue, and presented them as a means to grow the

business, but they didn’t sit well with King Bob, so they went nowhere.

The best I can hope for is that I can harvest some capital

gains from other investments when this business eventually fails so I can

offset the losses on my taxes.

In a future post, I plan to lay out the lessons learned from

this experience and hopefully it will help you, the reader, to avoid some of

our mistakes.

Post in the comments about your things that didn’t go right.

And, as always, let me know what you think in the comments.

Ask questions, tell your story.

If you like my posts, please share them with

others and subscribe to this blog.

Today I am going to do a review of Stessa, an online rental

property accounting platform.

But first, a disclaimer:

***This review may contain affiliate links that compensate me for user

registrations of this product.***

As I have detailed in a previous article, I started using Stessa

last year to track accounting for our rental portfolio. Previously, we used

Google Sheets, tracking rental income and expenses for each property on

different tabs. This would involve me going in to the first property’s income

tab, entering the collected rent, then checking all of my receipts and accounts

to verify I hadn’t missed any expenses and adding them to the expense tab for

that property. I set up expense categories and put in a section to summarize

the expenses by category and by month. While not ideal, it insured that someone

at my CPA’s office was not classifying an expense in the wrong category or for

the wrong property. It was not hard to do, just more a matter of remembering to

do it.

Around the middle of 2018, I started seeing advertisements for a product called Stessa on Facebook. As per my SOP, I ignored them, other than taking note of the name. A few weeks after first seeing the ads, I heard an advertisement for it on The Bigger Pockets Podcast. This was more effective, as they pointed out how it was free for rental property owners and individual investors and involved some automation to keep track of your accounting. They also pointed out how the product was developed by real estate investors for real estate investors and the name was “assets” spelled backwards.

I went to the web

site and registered for it. I was able to set up our properties and import

bank & credit card histories to the transactions section, allowing me to

categorize each expenditure. It took maybe 10 minutes to set up two properties.

And, once numbers had been entered, the dashboard populated with portfolio

metrics. Way nicer than my spreadsheets!

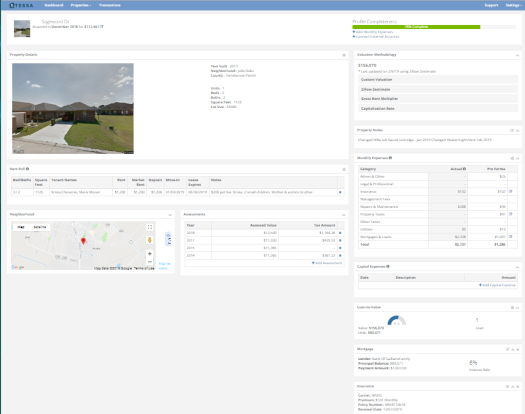

Features

Individual tracking for each property:

Property Profile

Header – Address, Acquisition Date, and Cost.

Property Details

– (Year built, neighborhood, parish [county, for those of you outside

Louisiana], number of units, bedrooms, bathrooms, square footage, and lot size,

all pulled from Zillow, based on the address.)

Valuation – Provides

for multiple options: Custom Valuation, Zillow Zestimate (automatically polled,

user choice to update property valuation), Gross Rent Multiplier, or Capitalization

Rate.

Rent Roll – Allows

entry of Bed/Baths, Square Feet, Tenant names, Rent, Market Rent, Deposit,

Move-in Date, Lease Expiration Date, and notes.

Property Notes

section – Freeform note space for property.

Monthly Expenses –

Allows for Pro-Forma expense entry and pulls in categorized expenses from the

Transactions section to show actuals compared to Pro-Forma.

Neighborhood –

Shows location on a Google map, with a Walk Score and a Bike Score for the

property.

Assessments –

Pulls in assessed value and property tax amount (I’m assuming from Zillow), and

allows you to add missing assessment/tax details.

Capital Expenses –

Allows for entry of Date, Description, & Amount of Capital Expenditure.

Loan-to-Value –

Shows a chart with LTV percent, Property Value, Debt (principal balance), and

number of loans.

Mortgage – Details

the Lender, Principal Balance, Payment Amount, and Interest Rate.

Insurance –

Displays the Carrier, Premium, Policy Number, and Renewal Date.

Transactions:

As I mentioned above, Stessa

allows you to link bank accounts and credit cards to the Transactions ledger.

It lets you initially import all transactions and gives you the option to

review them to either categorize each one correctly or, in my case, the credit

card I use also has personal charges, so it it allows me to delete those

transactions.

Stessa does not store your credentials on their servers and

use bank-level encryption to secure the transfer of information. It also does

not allow changes to your bank or credit card accounts. It only pulls a copy of

your transaction information.

The Transaction Ledger Menu allows you to review new

transactions, view ALL PROPERTIES transactions, view individual property

transactions, or add a new property.

The main Transaction Ledger display shows all transactions, filtered,

based on the menu selection. It additionally allows you to search by keyword

and/or filter by Date, Category, Amount, or Account.

There is also an export function, allowing you to export

filtered transactions to a *.csv file.

You can manually import *csv and *.qif files from accounting

software, in addition to adding individual transactions by hand, such as

mileage.

Reporting – Reporting is one of the reasons I was interested

in trying out Stessa in the first place. It provides you with standard reports

such as Income Statements, Cash Flow, and Capital Expenditures, with options to

select a date range, property/portfolio, monthly breakout, and whether or not to

show Category Details. The report is downloaded as an Excel file, allowing you

to customize the report title and report formatting, if needed.

The other reporting option I have mentioned before is the

Tax Package. This contains everything needed to hand off to your CPA at tax

time. And it sure makes it easier on me!

The dashboard is the main page you see when logging in on a

computer. It allows you to show the total portfolio or to select individual

properties.

It contains the following sections:

Portfolio Value – Options to see Market or Purchase Value.

Asset Return – Either Appreciation or Levered returns.

Occupancy – Detailed in percent.

Income

Cash Flow

Unit Count

Property Count

Debt – Total

Net Cash Flow – A chart detailed by month & Category

Location – Google map showing all properties in Portfolio

View or a single property in Property View

Compare Properties – Rental Income, Market Value, and Square

Feet. Available in Portfolio View only

Property Highlights – Property picture from Google Street

View, Income, Expenses, LTV, and Occupancy. Available in Property View Only

Summary

I think that Stessa is a great automation tool for rental property accounting. It’s free, cuts down on time spent doing bookkeeping, and makes tax time easier. On top of that, their user support is outstanding! Early on, I identified a couple of bugs and they were fixed within a couple of days. Amazing!

If you are interested in trying out Stessa for your rental properties, please click on the link below: