For the last 6 months, you have been getting to know a little bit about me through this blog. Now, I would like to know a little about you…or at least your thoughts on the blog and your interests.

So, with that, I humbly ask that you please respond to the survey at the link below.

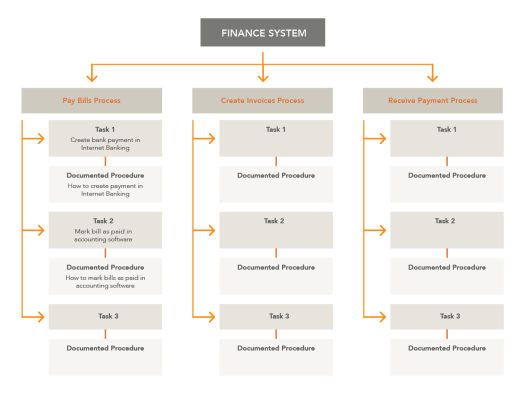

This week we are back to business basics. I am going to go over Business Processes, specifically, and why they are important to people running small businesses, better known as entrepreneurs.

Growing up, I yearned to run my own business. I was exposed to lots of people running their own businesses and it was seductive…do your own thing, be your own boss, make as much money as you wanted to (I was a poor kid and idolized the idea). But as I grew older, I would observe these various entrepreneurs’ businesses fail and disappear. Some of it was from bad financial practices, (as covered in this story: My History with Money, Pt. I), some of it was from just bad business ideas, but as I have come to realize, all of them were due to not having documented processes & systems in place to operate their business.

What is a Business Process?

A Business Process is a map of the steps needed to be taken to achieve a goal or result. This can be the process for generating a price quotation or making a Big Mac. It is the set of step-by-step instructions to complete that task.

It can be as simple as the process detailed below:

PB&J

Lay out 2 slices of bread

Spread PB on one slice

Spread Jelly of the other

Put the 2 slices together to complete the PB&J Sandwich

Or it can be extremely detailed, for quality control and efficiency:

Peanut Butter and Jelly Royale

Lay out 2 slices of bread that conform to the QC shape on the QC chart on the wall next to your station

Evenly spread 1 oz. of premium natural peanut butter on the right slice of bread

Evenly spread 1 oz of locally-sourced hand-made strawberry jelly on the left slice of bread

Align the peanut buttered slice of bread over the jelly spread on the other slice of bread and lower it to complete the sandwich

But What About Systems?

Some mistakenly refer to the processes and systems interchangeably. In reality, processes are part of a system. A collection of similar processes make up the system. Let’s you are running a fast food restaurant and you want to ensure that the food presented to the customer is the same, every time. You would document a set of processes for each item on the menu, similar to the PB & J examples above. This collection of processes would be your Food Prep System. You would have a separate system for taking orders and another for inventory, and so on.

Another point about systems is that a system does not have to involve technology. There have been lots of technology systems designed to ease and automate manual systems. An easy one to bring to mind is for accounting. You have many options available for electronic accounting systems, but it is still something that could be done by hand. Not that I am advocating to accomplish your accounting by hand. In most cases, using an electronic accounting system is much more cost-effective than doing your accounting by hand. In our real estate rental business, the accounting is handled using a Google Docs spreadsheet, because the complexity of what we are doing and the time it takes to do it does not yet justify actually paying for an electronic system.

Why do I Need Business Processes?

You may ask yourself “Why do I need business processes?” Well, if you are a sole proprietor, who plans to never expand, hire personnel, step back from working in the business, or sell the business, then you probably don’t need to worry about business processes. Even though you are most likely following business processes already, if the above description fits you, you can probably get away with not documenting your business processes.

If you don’t fit the description above, these are the main reason to document your processes:

Precision and Consistency – You want to ensure that things are being done the same way every time. Borrowing from the Peanut Butter and Jelly Royale example above, if you don’t specify how much of each material to use, then you are left with each order resulting in varying quality AND cost to you as the business owner or operator. While using more peanut butter on a sandwich sometimes seems like a small thing that can be overlooked, it affects your Cost Of Goods Sold (COGS) for that sandwich, and throws off your inventory, which could result in your running out of peanut butter before your next order. This could affect your sales of the Peanut Butter and Jelly Royale until you get more product in.

Even if you are able to go out and source a spot supply of peanut butter, it will most likely further impact your cost.

**For the purposes of this example, the peanut butter sandwich and it’s ingredients are a metaphor for whatever you happen to sell in your business**

Redundancy – It is a good idea to document business processes as a kind of back-up. The reasoning behind this relies on the “Hit By A Bus” theory…If the business process is not documented, how would someone else be able to accomplish the task if the person(s) who know how to do it should get hit by a bus?

Efficiency – By having the detailed steps laid out in a business process, there is less chance of deviation of how to accomplish the task, allowing it to be completed faster. The caveat to this is that the process must already be efficient. One way to ensure efficiency is to review processes periodically to make sure they are the optimal way to achieve the task.

Scalability – Another reason you need to have documented Business Processes is to achieve scalability. Let’s say your company builds a widget and you have an opportunity to lock down a sales contract to deliver 25 widgets a month. Your business historically has only delivered a maximum of 10 widgets a month. How do you scale up your business to be able to produce 150% more product? By bringing in more employees. How do you train the new employees to be able to accomplish those tasks? By having detailed Business Processes for you Widget Production System so that employees can get up to speed faster on how to do their job and allow you to produce that increase in widgets almost immediately.

I hope I have been able to make a compelling case for why you need to have documented Business Processes and helped you to understand how it can help your business.

Here is some recommended reading on Business Processes:

Contract Contingencies or “loopholes” can help you get out of a bad deal.

This week I am going to go over how you can be protected by contingency clauses in your purchase agreement contract, specifically from an investment perspective.

Purchase Agreement Loopholes

When you sign a standard real estate purchase agreement, you have the option to include contingencies, to protect you and allow you to get out of the agreement. You can include a financing contingency, (if you need to get approved for financing), a title contingency, (in the event the title is not “clear”, in merchantable condition, and the seller cannot remedy it), sale of another property, appraisal price being equal to or greater than the sale price, no issues found during an inspection period, or pretty much any other contingency you would like to include.

The key thing to remember is that the seller has to accept these contingencies. The specific ones listed above are standard contingencies and sellers are used to seeing them. As a real estate investor, you should know that the number of contingencies could possibly affect the seller’s decision to accept your offer if there is a similar offer for the property with less contingencies.

The main contingencies to include are the inspection period and clear title.

You should have your financing in place already, to make the deal go smoothly. This can be personal cash, private money, hard money, or being pre-qualified for a loan from a traditional lending institution.

In selecting your properties, you should have a pretty good idea of the market value of the property and in pursuing the target property, have negotiated a sale price that is discounted from market price, allowing you to cover expenses and cash flow.

Utilizing a Contingency

A couple of weeks ago, I posted about making an offer on an REO property. I was excited for the opportunity to acquire this property because it was in the same neighborhood as the last property we acquired and had a couple of more amenities.

We were at the point of waiting for the asset manager to respond with the final signed contract so we could start the inspection period. We waited and waited…but did not hear anything for a whole week.

We were told to expect up to a seven day wait for a response, but when we finally did get a response on the ninth day after we submitted contract signatures, the asset manager had signed the contract two days after we submitted it. This left us with approximately two and a half days for inspections, title search, etc., and late on a Friday morning. There was no way we would have been able to get the title search completed at that point.

We exercised the contingency and canceled the contract.

Because of issues like this, I am glad I had the option to exit the deal. Some investors may not worry about the title, but I do. I have run into title issues in the past that made it hard for me to sell a property, so I wanted to be sure that the title was clear. Especially with the property being an REO property.

With it having been through a Sheriff’s Sale, the title “should” be cleared of all liens, but if a lienholder was not notified that the property was going up for Sheriff’s Sale, then their lien is still in effect.

I could have run the title search before getting confirmation that we had a contract in place but did not want to spend $500 and not be able to get the property under contract.

So, on with the property search!

Oh, if you are in the Houma/Thibodaux area and have property you need to sell, get in touch with me.

And, as always, let me know what you think in the comments. Ask questions, tell your story.

If you like my posts, please share them with others and subscribe to this blog.

This week I am going to talk about how you send you time and how it affects progress towards goals. This is a topic that keeps coming up (for me) from various sources and every time it does, I get more of an urge to discuss this topic here. So…here we go.

“How do you spend your time?”

Ask that question of a hundred different people and you are likely to get a hundred different answers. Some people may list every detail, others may just give a twenty-thousand-foot overview.

Successful people have goals.

Successful people have a plan to reach those goals.

Successful people follow a process and their processes are habits.

Observations of Others

In a recent blog post, Dave Van Horn talks about a speaker at a recent investing summit who asked the question “What would you do if you were a billionaire?”

The answers were some form of the three below:

“I would travel more.”

“I would focus on my passion.”

“I would give to charity.”

Dave then goes on to point out that “billionaire” status is not needed to achieve these goals, as evidenced by the speaker, (not a billionaire), only that you budget your time as you do your money to its best possible use. Don’t waste your time doing things that won’t move you forward. You can pay someone to take care of that for you if your time would be better spent being effective.

He then relates how Tony Robbins asks similar questions:

What is an extraordinary life for you? – Hopefully this is something that you can achieve in the next six to twelve months.

What is preventing this from happening already? – What story do you give as an excuse for not having achieved it already?

What needs to change now? – This brings it back to taking action.

This may sound familiar. It is similar to what I outlined in how to resolve overspending.

Once you have set a goal, identified what is stopping you from achieving that goal, and put a plan in place to change things your goal, things may still not happen perfectly.

Life will always throw you curveballs. Our initial reaction is to get emotional and point to all the reasons why we are failures. We can come up with lots of feelings on the subject, but in reality, over the long term, they don’t make much of a difference in the long run. Life goes on.

The way we can get through this is to put it in perspective. Learn from failure. Defeat your emotions with logic. What important things are you missing because you choose to worry versus logically evaluating the facts? Just because you are in control of your emotions does not mean you don’t feel them, just that you are taking care of business so you can deal with your emotions at an appropriate time.

By thinking clearly rather than getting caught up in emotions, General Eisenhower, in WW2, was able to determine a way to defeat the German Blitzkrieg, a battlefield strategy that involved throwing everything they had at the allied forces in a single attack. It was scary and worked in lots of battles, with allied forces so surprised, shocked, and overwhelmed by the speed and ferocity of the attack, that they just gave up.

General Eisenhower realized that the Germans were putting everything they had into the attack, leaving their flanks and rear unprotected. His approach let the Germans attack, but held groups back to flank the German attack, thus surrounding & defeating them.

Here are some quotes that reflect this approach that I find helpful:

“What doesn’t kill you, only makes you stronger!” – Jean-Baptiste Emmanuel Zorg (Antagonist from The Fifth Element)

He wasn’t the originator but is as good an attribution as any. This means that you learn from your mistakes. Dealing with difficulty helps you to become more resilient, more anti-fragile.

“I must not fear. Fear is the mind-killer. Fear is the little-death that brings total obliteration. I will face my fear. I will permit it to pass over me and through me. And when it has gone past I will turn the inner eye to see its path. Where the fear has gone there will be nothing. Only I will remain.” – Frank Herbert, from the book Dune.

It is OK to be scared, but don’t run from it. Face your fears. Once you face your fears, they have little power over you.

“Our actions may be impeded, but there can be no impeding our intentions or dispositions. Because we can accommodate and adapt. The mind adapts and converts to its own purposes the obstacle to our acting. The impediment to action advances action. What stands in the way becomes the way. – Marcus Aurelius – Holiday, Ryan. The Obstacle Is the Way: The Timeless Art of Turning Trials into Triumph (p. 1). Penguin Publishing Group. Kindle Edition.

This is similar to the “What doesn’t kill you” quote but goes a little deeper and touches on something that doesn’t seem common these days…the idea that by facing hardship, you grow. In fact, it is the reason for the title of Ryan’s book, “The Obstacle is the way”.

Do the uncomfortable things, if it will further your goals.

Grow from those experiences, so that next time, you either know how to handle it already, or if it is a big issue, avoid it altogether.

Learn from mistakes.

Budget your time.

Budget your money.

Grow, as a person and as a leader.

And, as always, let me know what you think in the comments. Ask questions, tell your story.

If you like my posts, please share them with others and subscribe to this blog.

Yes, you can legally sign digital documents from your phone!

Today I am going to go over how we negotiated a purchase agreement for a new rental property while we were on vacation. I will summarize how it can be done and why you shouldn’t sit around waiting for something.

REO? (Not Speedwagon)

Part of my process for finding properties is to have searches set up on the various real estate websites such as Trulia, Zillow, and Realtor. They send me emails on a daily basis with local properties in my areas of interest that meet my investing criteria. I noticed that there was an REO property up the street from the last property we purchased. REO is Real Estate Owned and means that it is a property that the bank has foreclosed on and wants to get off of it’s books, hopefully recouping the money they have into it.

This property had been foreclosed on by the bank and sold at a Sheriff’s Sale back to the bank at some point prior to February of this year. They then listed it for $98,800. About six weeks later, they dropped the price to $89,900. A month later, it was $79,900. Then they ramped it back up to $98,800 after 6 weeks, but dropped it to $79,900 about 5 days later, so it must have been a typo. And roughly two weeks after that, they dropped the price, again, to $69,900.

It was at this point that we decided to go look at it. There was no power or water service connected, so we couldn’t inspect the plumbing or electrical functionality, but we were able to look at everything.

The property apparently had doors and paint updated in recent years. The floors were mostly tile throughout, with real parquet wood floors in two of the bedrooms and damaged/improperly installed laminate flooring in the master suite. The back exterior will need a little attention along with the roof, but all in all, the property appears to be in good shape and not needing as much in rehab as our last acquisition.

The Rub

The day we looked at the property was the day before we were leaving for the week to go on vacation out of state. We did not have time in our schedule to travel to the realtor’s office and sign paperwork. Luckily, we did not have to. The offer was submitted online via a secured signing portal.

All further counter-offers were done in a similar manner either from my phone or laptop, allowing us to enjoy our vacation and still take care of business on our schedule.

We are currently waiting on the “paperwork”, but we have come to an agreement on price and are waiting for the start of the due diligence process, where we get the property inspected and look for any deal-breakers.

I will detail the whole deal in a future post, once the deal is complete and the property is rehabbed and rented.

And, as always, let me know what you think in the comments. Ask questions, tell your story.

If you like my posts, please share them with others and subscribe to this blog.

Today I want to go over Cash Flow and why it is critical to business finance.

There are four basic reporting metrics for business finance:

Balance Sheet – Statement of financial position, reporting a company’s assets, liabilities, and owners’ equity at a given point in time.

Income Statement – Statement of revenue and expense or profit & loss.

Equity Statement – Statement of changes in equity or retained earnings.

Cash Flow Statement – Statement of a company’s cash inflows and outflows during a given period of time.

I will cover the first three in more detail with later posts because I want to talk about Cash Flow and the Cash Flow statement.

Cash Flow

Cash Flow is the total amount of money coming into a business (revenue, income, investments, loans, etc.) and the total amount of money going out of a business (bills, expenses, wages, capital purchases, etc.) over a given period of time. It can be a year, a quarter, a month, or any time period you want to look at. For my purposes, monthly reporting is preferred, as it coincides with other regular monthly financial reports.

Doesn’t the profit & loss report show you the same information?

While reporting similar information, Cash Flow & Profit & Loss Reports serve different purposes. The Cash Flow report gives you an understanding of how you are bringing money into your business and how you are spending it while the P & L report shows you revenue earned and expenses paid.

OK, that still sounds similar, you say.

It may be easier to understand if you look at it from the perspective of different accounting methods. Businesses use either the Cash Basis or the Accrual Basis methods.

If you are operating on the Cash Basis method, your revenue and expenses are recorded into your accounting system when they occur. In this case, your P & L and Cash Flow Reports should show almost the same information for a given period, with minor differences like loan principle repayments not showing up on a P & L.

In the case of the Accrual Method, you might earn revenue in a given month, but you won’t see the money from it until the invoice gets paid, which may be a month down the line. As for expenses, you may be paying for supplies immediately, but can’t show them on the P & L until the revenue is earned. So, you are potentially paying for supplies in one month, showing revenue in the next month, and not actually getting paid until the third month. In this scenario, the P & L would show the expense & revenue in the second month, but the Cash Flow would show the outflow of the expense in the first month, no activity (with respect to the subject order) in the second month, and would show the revenue inflow (invoice being paid) in the third month.

Because of this, you should be looking at both reports to better understand what is going on in the business.

Why is Cash Flow important?

To be a successful business, you want to have positive cash flow…that means that you have more money coming in every month than you are paying out in expenses, wages, and bills. This seems like a “DUH!!!” statement, but without looking at both your P & L AND Cash Flow reports, it would be hard to make sure you are able to bring in more cash than pay out in expenses.

Without regularly reviewing the Cash Flow statement, you might think you are breaking even or close to it, until you realize that your bank account has steadily been dropping and you really were not even close to breaking even.

And, as always, let me know what you think in the comments. Ask questions, tell your story.

If you like my posts, please share them with others and subscribe to this blog.

This week I am going to discuss Accountability. I feel that understanding accountability is very important for succeeding in life. My grandfather told me that I have to be accountable for my actions and words when I was about 10 years old. I have tried to be true to that principle throughout my life.

After he passed away, a few years later, I figured out another lesson…that you should not rely on anyone else to guarantee your success.

The expectation was that we would all, (the grandchildren), continue in the family seafood business. I soon realized that I couldn’t depend on people’s promises to get ahead. That if I wanted something, I had to make it happen myself.

Because of my decision to take control of our future in the last few years, I started a journey of self-improvement. I have learned a good bit and implemented many of the things I have learned. Some things I was already doing, others were revelations. Below is a brief, non-exhaustive summary of what I have learned.

Be Accountable to Yourself!

Decide to Change

Nothing you want to change will change until you decide to change it. Griping and complaining about how bad a situation is will do nothing about it. Saying you will change or want to change will do nothing about it. Until. You. DECIDE. To. CHANGE.

Set Goals

Set goals you want to achieve. Things you want to accomplish. Places to visit. There are a couple of different ways to approach this. One is to take the bucket list approach. Detail everything you want to do. Tim Ferris suggests writing daily goals on a quarter-folded sheet of paper. This way, the list stays small and achievable. Whatever approach you take, remember this:

“Alice: Would you tell me, please, which way I ought to go from here?

The Cheshire Cat: That depends a good deal on where you want to get to.

Alice: I don’t much care where.

The Cheshire Cat: Then it doesn’t much matter which way you go.

Alice: …So long as I get somewhere.

The Cheshire Cat: Oh, you’re sure to do that, if only you walk long enough.”

Based on the above, unless you have a goal, you can’t really direct what you are doing. Which leads us to the next step…

Make a Plan

Once you have your goals in place, put together a plan on how to achieve them. Figure out what you will need to do, in the most efficient order you can think of. Try to mitigate risk by thinking of all the bad things that could happen along the way and have a plan for dealing with them.

Find an Accountability Partner

A lot of advice I have run across recommend having an accountability partner. Someone to express your goals to, review them on a regular basis, and help to keep you on track to succeed.

Grow! Achieve! Succeed!

All that is left to do now is to proceed…OK, it’s not that easy, but, the thing to remember is that you will run into setbacks. Things will go sideways every once in a while. Do not let that discourage you. Keep pushing forward and be the YOU you want to be. Like Mike Tyson said, “Everybody has a plan until they get punched in the face.” Learn to be resilient. Take responsibility and move forward, ever forward.

http://www.thatonerule.com/

And, as always, let me know what you think in the comments. Ask questions, tell your story.

If you like my posts, please share them with others and subscribe to this blog.

Saving Money…Maybe you should think of it as Rescuing Your Money!

This week I am going to cover saving money. There are many differing thoughts about this topic these days, some of which have valid points. I will also lay out my thoughts on the idea.

Saving Money – Why Should You?

Why should you save money? You can save money for an emergency. You can save money for to buy something special. You can save money for a dream vacation. You can save money for retirement. Your reasons are valid for you.

Tim Ferriss advises that you set dreamlines…goals you want to achieve and figure out how much it will cost, both per month and one-time charges, so you can figure out how to get your retirement now rather than delaying and saving for “one day”. There is also this whole part about coming up with a muse, or business idea that will provide the extra income to cover the costs of achieving that mini-retirement. The other thing is that they should be frequent.

Robert Kiyosaki says “Savers are Losers!”. His reasoning is that no matter how you are saving money, be it in a bank, in a Certificate of Deposit (CD), or in a pickle jar buried in the back yard, you are losing money, at least at this point in time, because of monetary inflation.

Why under the mattress, In a savings account, or In a Certificate of Deposit Costs You Money

Currently the rate of inflation is approximately 2%. Based on the definition above, that means that your money loses 2% of its purchasing power. If your savings account is paying 0.25% interest rate, your money in that account is losing 1.75% with this rate of inflation. If your CD is paying 0.3%, you are losing 1.7%. And if you have it in a pickle jar, you are losing the full 2.0% of purchasing power by not doing anything with it.

Ultimately, as far as I am concerned, instead of just saving money, put your money to work in an investment that will earn you more than the rate of inflation. Historically, the S&P 500 has provided positive returns over the long term, but in some years, like 2008, it had a negative 37% yield.

Overall, accounting for inflation, the market seems to average about a 7% return, but you will be advised to leave your money in the market and let things work themselves out. We have money in the market in the form of traditional & Roth IRAs, regular managed investments, my 401k, and various individual stocks that I play with (not very much).

I, personally, don’t want to devote my time to attempt to master the market.

Why you should make your money work for you

We also are investing in real estate. So far, those investments are working out to about a 9% return. Real estate has many options from flipping, to buy and hold (rentals), to lending, to investing in notes (becoming the mortgage holder for other borrowers). As stated before, BiggerPockets is the best free education on real estate investing you can find.

Additionally, we invested in a high-end door manufacturing business. It is not currently providing a return on investment, but it is improving and still self-sustaining, in addition to providing me and my fellow investors with some of the best business management lessons we have ever run across.

The bottom line, make your money work. To paraphrase the old adage, if your money is not moving forward, it’s falling behind.

And, as always, let me know what you think in the comments. Ask questions, tell your story.

If you like my posts, please share them with others and subscribe to this blog.

The paper details a study by Pason, a company that collects, analyzes, and distributes real time and historical drilling data from rigs in North America. They conducted a study on the accuracy of Weight On Bit measurements and determined that the majority of the WOB data was incorrect due to drillers not properly zeroing the WOB indicator. They proceeded to develop an automated algorithm that zeroed the WOB and another key measurement, differential pressure. This improved the accuracy of the data collected immensely.

The thing in the JPT article that caught my eye was the question, paraphrased here, “What is keeping the industry, as a whole, from collecting more accurate data?” The main answer seems to be that collecting more accurate data is not free. Due to needing to utilize more accurate sensors and having, at minimum, personnel regularly recalibrate those sensors, to developing better sensors and systems, it all costs more money than the current standard provided.

This is a parallel to what we are seeing as a hindrance to progressing with Drilling Automation. Operators want the lowest price they can get to drill their wells, service & equipment providers want the highest price they can get for their equipment, products, & services, and in most cases, what you wind up getting is low-cost provider solution (read minimum quality for cheapest price).

In recent history, most operators have not wanted to help develop new technology and/or practices. While you do see companies like Statoil, Royal Dutch Shell, Apache, and others investing in drilling automation projects and sometimes partnering with service providers to do this, the majority do not.

I think part of the reason why we are not seeing large scale advancements with Drilling Automation is that there is not one entity in control of the entire operation. Factory automation is far easier for at least two reasons: Factories are usually controlled by a single entity and the tasks that are automated are simple, repeatable steps.

Drilling a well is not the same as operating a robotic factory. You can automate a lot of things that are repetitive and can be accomplished by robots. Drilling a well is not the case. There are exponentially more variables involved with drilling a well than welding pieces of a car together. Due to that expansive number of variables, changes in each multiply the contingencies and potential responses needed. To sum it up, it is not an easy task to accomplish. Not impossible, mind you, just not easy.

A lot of wells involve a minimum of three or four different companies working to drill the well. All with different goals and business models. That adds to the complexity. This can be somewhat caveated by Red or Blue rig models where a single service company provides most or all of the various services to the operator on the rig, OR the independent Operator model where they hire their own consultants and utilize third-party suppliers for equipment & products.

So, because of all this complexity, in addition to variations in the market (read: Current, hopefully over, crash in the industry), it makes it hard to make progress with drilling automation.

BUT, there are changes afoot! Industry conferences are starting to highlight Drilling Automation. More companies are becoming involved in the space. With the progress being seen in artificial intelligence, things that someone had to “feel” or “intuit” may soon be reduced to a routine validated by a computer algorithm.

We are starting to see progress. Interest from multiple players, large and small. Companies transferring their expertise from wetware to hardware and software. The singularity for Drilling Automation is not tomorrow. We may never get to a totally automated drilling process with no human involvement, but if we can get 95% there, that will be a huge reduction in cost and increase in efficiency!

And, as always, let me know what you think in the comments. Ask questions, tell your story.

If you like my posts, please share them with others and subscribe to this blog.

Today we are going to talk about a very specific subject: Starting a small business with a partner or partners.

The generally understood definition by the United States government for a small business is a business that employs less than 500 people. There are financial considerations that also go along with that, but I am not going to attempt to touch on those here.

With this in mind, the concept of the US economy being powered by small business makes a lot more sense. A large majority of businesses are small businesses.

I would venture to say that there is a sizable portion of the population that if not already running a business, want to start one. Based on that, I am going to provide some tips to get started and hopefully avoid pitfalls that I have run across in my business dealings.

Partners

Select your partners well. This seems obvious, but you need to ensure that goals are aligned, that you want the same things for the business. Make sure that you can work with your partners. Make sure that your personalities do not clash. Make sure that all partners are able to understand viewpoints that are different from their own ideas and give them thoughtful consideration. Put a plan together for how you will proceed and have everyone sign off on it. Avoid partnerships where one or more partners are self-serving and attempt to obstruct ideas that do not favor them.

Duties

Define the duties of each partner for the business before investing any money, time, or effort. Agree on who does what and how it will be done. Have each partner provide a plan for how they will accomplish their duties. This seems a bit like overkill, but the effort put into this exercise will pay dividends in the form of getting each partner to think about what they will be doing and how they will be doing it. That alone is worth the exercise.

LLC or C-Corp

There are other types of legal entities, but this seems to be the most common structure used for small businesses. Depending on the type of business, you may be forced into using a C-Corp entity structure, such as a manufacturing business with inventory. While I am not an attorney and I do not play one on the internet, I am of the opinion that most small businesses are best served by an LLC structure.

In an LLC structure, the entity is considered a pass-through entity, so the profits of the company are passed through to the partners based on shares of equity in the company, to be reported on their personal income taxes.

With a C-Corp, the company is taxed, then dividends passed on to the shareholders (partners) is taxed again.

Operating Agreement

This is also a big one. The operating agreement can be based on the details pulled together in the Duties step. It just formalizes how the company will operate and documents the what & how for each partner. It also should contain exit strategies for each partner and for the company as a whole. This is probably more geared towards an LLC entity, but also has relevance to shareholders in a small private C-Corp.

Entity Name

If you already have a good idea for an entity name, then obviously, use it. But if you don’t, there is no need to stress out over it. Pick a name and as long as it is not already in use or trademarked, it will be good. If you later want have specific company branding/marketing, you can create a “Doing Business As” or DBA name. In most cases, all you have to do is file a form with the state for it to be recognized.

Employer Identification Number (EIN)

The Internal Revenue Service (IRS) uses the employer identification number or Tax ID as an identifier for businesses so they can track income and revenue. It costs nothing and can easily be applied for online.

Business License

Depending on the nature of your business, you may need to get a parish, county, or city business license. They are usually just a nominal fee, but not a whole lot. (Caveat: larger cities may have more exorbitant fees).

Business Bank Account

Always use a business bank account for your business finances. Keep your personal finances separate from your business finances. This will help to keep track of how well your business is doing.

Accounting

For accounting purposes, you can start out tracking everything in a spreadsheet. Document revenue, document expenses. Depending on the nature of the business, you may need to do a little more than that and use an accounting software program or service. Once you reach a level where revenue and cash flow allow it, accounting tasks can be delegated to a book keeper.

I would also like to recommend using a CPA for filing your taxes. Having a good CPA on board will keep you out of trouble. Especially if a partner decides it is someone else’s job to get all documentation to said CPA at tax time. The CPA will file an extension on your behalf to keep you out of trouble.

And, as always, let me know what you think in the comments. Ask questions, tell your story.

If you like my posts, please share them with others and subscribe to this blog.