I worked in the oil and gas industry from 1992 until 2020. During that time period I was involved in a couple of real estate deals/activities, but really did not start to focus on investing in real estate and businesses until 2016.

Part of my departure from oil & gas was to move into real estate sales. It was once of the best things I have ever done!

I enjoy Sci-Fi, Epic Fantasy, technology, and music.

My superpower is that I have the ability to visualize how to make disparate parts into a working system.

I think my greatest failing is that I have trouble focusing on one thing.

I live in South Louisiana with my beautiful wife and two wonderful daughters.

How are you doing? How are you handling the mis-named “social distancing”? We are going a bit stir-crazy. I am probably more used to the isolation and not being able to go anywhere from when I worked offshore in the oil and gas industry. This is a lot nicer than sitting on a floating rig that you have to fly for one to two hours in a helicopter to reach.

Feel free to reach out if you need to talk to someone. It actually helps with the isolation.

Now, on to the content…

Due to the statewide Stay at Home order here in Louisiana, our local REIA are not able to get together for our monthly meeting. So, I’ve decided to move it online, replacing it with a livestream. Since it covered topics that I think are relevant to a larger audience, I’ve decided to share it with this community, too.

In this video, Tim Blanchard, of Allegiance Home Lending, discusses how mortgage rates work, what the impact is from the Q1 2020 FED Interest Rates on mortgages and regular loans, and gives advice on utilizing SBA Coronavirus relief options.

Things you will learn in this video:

What affects mortgage rates.

What mortgage rates are based on.

What drives a change in mortgage rates.

How Lenders’ Credit Score Criteria have changed in this environment.

SBA Coronavirus relief opportunities for businesses.

Today I’d like to pass on something I have shared in our local REIA group with regards to working with your tenants during this time of crisis, especially if they have recently become unemployed or furloughed.

If you have rentals and have not done so already, it might be a good idea to reach out to your tenants and check in with them. Due to various business shut-downs, lock-down, and stay-at-home measures, they may have become unemployed. Depending on their financial situation, it may make it difficult for them to pay their rent.

Below is a copy of what we sent out to tenants:

Hi, Tenant

How are you? We hope you and your family are staying healthy and getting by at the moment. While I don’t know exactly how the coronavirus situation has impacted you, I’m sure it has not been easy. Personally, my family and I are going a bit stir-crazy, but are taking the down time to ride our bikes and totally redo our landscaping, (who needs the gym, right?)

I imagine you are spending more time more time at home than usual, given the current circumstances. Maintenance people are tough to schedule right now due to safety concerns, but please do not hesitate to reach out if there are any maintenance issues so we can make your your extended time at home more comfortable.

If you have any other needs or issues, again, do not hesitate to contact us.Below is a link to a list of resources that may be helpful during this trying time:

Since we currently cannot conduct eviction proceedings, (and to be honest, this is not the time to be evicting people unless you were already planning or in the process, more on that in a bit), I think it would be best to work with your tenant to see what they can pay, and accept that with the understanding that the balance is still owed. You can work out a repayment schedule over, say, 10 months or so, starting in May. This gives the current craziness time to settle down and should make the payments small enough so that it does not wreck their budget. This assumes your tenant is staying with you long-term.

Additionally, you should get this repayment agreement written up as an addendum to your lease. This will provide a paper trail of it.

***DISCLAIMER*** I am not an attorney and I do not play one on the internet. Please consult your attorney for proper legal phrasing.

Now, if you were already in the process of evicting someone or preparing to, one option you can try is “Cash for Keys”. This is obviously not without cost, but could possibly give you a quicker resolution than waiting to evict them. The way cash for keys works is that you offer the tenant you want to leave a lumps sum dollar value to vacate the property, leaving it in undamaged clean condition, within a certain number of days. You frame it to them as something to help them find a home that better suits them. And, unless there is already a lot of damage to the property, give them back their full deposit to expedite the process. This will help to keep them from damaging the property before leaving.

Merry Christmas! Happy Holidays! Happy Solstice! Happy Hanukkah! Joyous Kwanzaa! Yuletide Greetings! Joyeux Noël! Feliz Navidad! Season’s Greetings! Happy New Year! Joy! Celebrate! Be Merry! And most of all, wishing all of you who read this a new year full of peace and joy!

I’m sitting here between Christmas and New Year’s Day contemplating the future. To paraphrase Game of Thrones, “Change is Coming”.

As many of you know, we decided to start investing in real estate as a buffer to the ups and downs of my chosen industry, Oil and Gas Exploration. I was able to make it through some of those ups and downs in the past, maybe by luck, or because what I was working on was important. At one point, I did take a demotion and worked in the field (offshore, on the rigs, for about a year, but was able to move out of that role and on to greater things.

Which brings us to current times. Things have dipped again.

I usually take the last two to three weeks of the year off since I usually don’t use all of my vacation throughout the year. I was sitting at home and my supervisor called and asked if I was at the office. Since I wasn’t, he asked if I could come in. This told me that something was up because his office is over 100 miles away and if he is at my office, then it must be my turn.

And it was, but with a twist. I was offered a choice between an early retirement package or a rotational position working in Houston.

My darling wife and I contemplated the choices for a couple of days. Ultimately, we decided that it would be best to take the position in Houston. While we would be OK with me not working for a while, ultimately, it was our need of medical insurance that swayed our decision. Speaking of medical insurance, my next article will cover my experience in trying to get a quote for it and the fraud potential inherent in the Louisiana Medicaid Program.

Working a rotational job in Houston would mean finding a place to stay when working and time away from the family, but it also would mean that for two weeks out of every four, I would be off of work and free to do as I please.

This should allow for catching up on projects around the house and more opportunity to generate passive income.

The down side is that I will not be in town for some of the Bayou Real Estate Investor Networking meetings. I will continue to organize them, but will have to rely on other members to host when I cannot attend.

Additionally, if any of you live in or around North Houston / Humble / Kingwood and know of decent rentals at a good price, please contact me!

And, as always, let me know what you think in the comments. Ask questions, tell your story.

If you like my posts, please share them with others and subscribe to this blog.

Actual Numbers. Blanks are where numbers were not needed.

Today’s topic is about reviewing your insurance coverages and ensuring that you are properly covered at the best rate. It also touches on customer service and some things that caused me to look for a change.

Isn’t it crazy that it is December already? The end of the year, the end of the decade. Here at the Galliano household we are busy buying Christmas gifts for the family and coordinating our schedules for band concerts, choir concerts, and a birthday.

It is also about paying year-end bills…we have property taxes on our rentals, but that is covered easily by the rent. We also have property taxes on our residence and another property. We can’t do a whole lot about what we are paying on those taxes.

Then there is insurance. Since we paid off our mortgage years ago, we have to purchase homeowners’ insurance outright. AND, since we originally moved into our house right before Christmas, our insurance comes due at Christmas time.

On top of that, our auto insurance is due on 02-Jan-2019. So that totals up to a lot of bills at the end of the year.

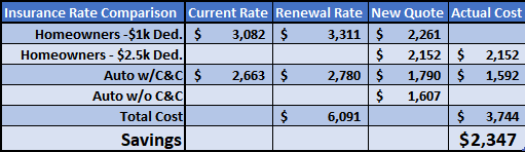

The current (as of this writing) agency we use has been providing me with insurance for around 20 years. But I am not happy with them. Over the last four to five years, my “agent of record” has changed at least four times. And the only way I find out about it is if I call with a question. On top of that, when the renewal notices came in this year, they totaled to a little over $6000! I asked for a quote at a lower home value, because the company we are covered with has an auto-escalate policy and increases the coverage value every year, thus increasing the premium. The renewal value was for $291,000. My home is probably worth about $250,000 on a good day.

I also asked for an increased deductible, increasing the deductible from $1000 to $5000. They couldn’t do that. They could only do two percent. So I asked the agent to quote me for coverage on a more accurate home value. Two to three days later, I get a quote for a home value of $232,000. Yes, it was $1000 or so cheaper than the renewal quote, but it was not for the home value that I requested. Because of this, my search for a new provider began.

One of my fraternity brothers offered to give us quotes. In going through that process, we were able to get the coverage we wanted at much lower rates. Between the home and auto coverage, it only cost us $3,744, for a savings of $2,347 between the two. That is almost $200 per month of savings! That will cover a trip to Disneyworld for Mardi Gras! LOL

Tips for Insurance

Below are some tips for getting the most for the least when dealing with insurance:

Review your policies annually to ensure accurate coverage – Make sure you aren’t paying for a home value above the replacement cost of your home

Try to pay your policy in a lump sum – Some providers will give you a discount for paying in full

It pays to shop prices every once in a while

Ensure you have a good relationship with your agent – Find an agency that provides you with a single point of contact and will notify you of any changes

Your home value is not your home replacement value

Depending on the age of your vehicle, you may not need comprehensive and collision insurance

Be in a financial position to be able to pay your policies lump sum

And, as always, let me know what you think in the comments. Ask questions, tell your story.

If you like my articles, please share them with others and subscribe to this site.

Today, we are going to continue where the last article left off. We are going to go over the lessons learned from my experience buying a business with partners. I will list them out with short descriptions. There is no particular order to the list. Any names mentioned other than my own have been changed to protect the innocent…

Lessons

Learned

Partners (The Team) –Our team consisted of four partners. Bob and Carl are the majority investors and took out an SBA loan to acquire the business. John and I are minority partners and not party to the SBA loan. Because Carl, John, and I all have full-time jobs and at the time Bob did not, the plan was that Bob would learn and operate the business until we could afford to put someone else running the business, leaving Bob to pursue his personal interests. See my last article for how that all turned out.

Recommendations:

Be transparent about

individual drivers. Becoming your own boss and becoming wealthy eventually

become competing interests for an entrepreneur.

Professional respect

is critical. Tolerance is listening to every idea quietly. Professional respect

is availability, transparency, punctuality, and preparedness.

Autonomy must be

earned, never assumed in a partnership.

Bad habits are hard

to break in others.

Operating Agreement/Bylaws – Depending on whether you have a Limited Liability Company (LLC) or a Corporation (Co), you should have either an operating agreement or bylaws to govern how the business will be run. In our case, since we had a corporation, we had bylaws. We deliberated on what to include in these bylaws to ensure smooth operations, but did not go far enough. They did not spell out the duties of each partner & role, because we thought that all of us being adults, we would do what was needed to be successful. What we realized was that we each viewed the word through a very personalized lens and what seems obvious to one, (or two, or even three), is not obvious to everyone and if the fourth person feels strongly enough about it, they just will not go along unless forced to. And even then, although begrudgingly agreeing in discussion, they will still fight and obstruct the wishes and decisions of the group. If we had, as a group, decided on the duties for each role and assigned responsibilities for each role to each member of the group, then documented it in the bylaws, it would have made things a lot clearer.

Recommendations:

The operating agreement or bylaws should also include a

defined exit strategy that everyone has agreed to and is committed to

following. It should have defined triggers that initiate the exit strategy.

These triggers should be something that the partners can easily monitor and

measure against.

It should also be spelled out how to handle decisions and

requests. In our case, decisions initially required unanimous board approval.

We amended the bylaws later to only require a two-thirds majority due to the

one partner asking for a solution to a problem, but not liking the board

recommendations, then never implementing the solutions.

Due Diligence – Nowhere near enough due diligence was done on this business or partners. We did not understand enough about how either operated. The revenue the company was making included the previous owner doing work on weekend “off-book” to get jobs out & keep expenses down. It also relied heavily on promotion via owner visits with distributors and their personal relationship. We had no relationships.

Additionally, having a partner who tells the group he agrees

with the intention of not taking any profits for three years, but assigns

himself a $100,000 per year salary and in the first week of operation directly

violates the ground rules we set up for operating the business. We, (the other

three partners), realized that the fourth partner had pursued the investment

deal to set himself up with a kingdom where he was king. #AvoidDat

Recommendations:

Know how the business operates prior to purchase.

Calculate how much revenue you need to make to break even.

Have a budget that takes into account ALL costs to operate.

Unless you are laundering money for drug cartels, whatever

starting capital you have isn’t enough.

That much isn’t enough, either.

Planning to grow? Triple the previous statement.

Financials –While we started out with modest working capital, we had no understanding of our run rate, break-even point, or runway length. In other words, we did not know how much it cost us to operate, how much we needed to make to break even, or how long we could operate with the amount of working capital we had. We eventually figured those things out, but not until it was too late. Also, another point to make, as referenced in a previous article, you have to pay attention to Cash Flow to stay on top of your business finances. We utilized the accrual method of accounting, but did not regularly look at the cash flow reports. Because of this, we would account for interest paid on our loan from the Income Statement (P & L), but did not account for principle repayment in any of our break-even or forecasting exercises until almost two years into the business.

Recommendations:

The person managing the business needs to have a fundamental

understanding of basic accounting and business / financial principals. This is

a KEY point and will lead to many headaches if not followed.

Know your costs to operate, to the penny! AND, make sure you

include labor!

Cash is King! When you run out of working capital, that is

pretty much the end of the business.

Gross margins should be higher than thirty percent. If not,

this will lead to a death spiral for the company.

Sales – The business we purchased operates, (soon to be preterite or past-tense?), conducted sales via a convoluted structure. The products are sold via distributors to building supply centers for builders. So if an end user wants to use our product, they get their builder to point them to their preferred building supply store, where they can look at brochures or in some instances, floor models to decide on what they would like. They then request a quote. That request comes to our operation, is processed, and returned to the building supply store salesperson. That salesperson has limited information on the product nor incentive to sell it.

From our end, we pay a commission to a sales agent to

promote our products to the distributors, who in turn make them available in

building supply stores. This is too far removed from the end buyers and in my

opinion, not an effective spend.

Recommendations:

Agencies DO NOT replace effective sales people! Agencies

represent a large portfolio of products and do not focus on pushing your

product(s) 24/7.

It doesn’t matter what your product is if you and your team

cannot sell the product(s). No sales = No revenue = No profit = bankrupt

company.

It does not matter how much you cut costs or control

spending if you and your team cannot sell the product(s). (See equation above)

Operations / Efficiency – Prior to closing the deal on the business, since Bob was going ot be operating it, we requested that Bob create a budget and document processes for what the business would need to run. He never gave us a budget, nor processes, even after being in the business for a couple of years. His initial excuse was that he had to be working IN the business to understand how the business operated (for processes) and that we, as the board, should be giving him a budget that he could spend. These were two more missed #RedFlags in our journey that should have told us to run, not walk, to the nearest exit. As of today, there are still no documented processes. We kind of have an idea what our budget is through reviewing financials, but we don’t trust the numbers because they are constantly being adjusted. So, we only have an idea, and nothing from Bob. Ultimately, there are still a lot of inefficiencies in the way the business is being run.

Recommendations:

Inefficiency is

expensive and cripples or kills a company. From the start, focus on efficiency

of process, capital, communication, and decision-making.

Be deliberate and

realistic about growth rate. In projections and practice. Year over year

revenue and product volume increases have to be realistic and managed to avoid unmet

expectations and quality issues. It’s nice to have targets, but remember that

you need sales to support targets (see Sales section below). And it is much

easier to have a customer wait for quality than to apologize for a sparkly

piece of crap.

Product Management –This business has about eight main products with practically infinite levels of customization, not counting special-order material types. Every order is a custom order with many options to choose from. There are forty-five different options to choose from when requesting a quote. This leads to decision fatigue and indecision in customers. Ultimately, our quote/win ratio was very low. We suspect that most customers that requested a quote had already decided on something else by the time they received the quote back. Additionally, “Bob” was continuously wanting to add new products to the portfolio because they were the latest hot thing selling.

Recommendations:

Have IP, a unique desirable product, or both. If you have

neither, shoot it in the head, kill the deal, pull the plug, or whatever

euphemism you want to think in. Unless your goal is to be your own boss, then

feel free to limp along for eternity (or until your cash runs out).

Keep or reduce your product line to your top sellers. Based on the Pareto Principle, roughly 80% of your business should come from your top 20% of sales. (Just a note, it will not be exact. This is a rough guideline) So, find out what products make up the majority of your revenue if you already have a large portfolio of products and focus on selling those products. If you only have a few products, keep this idea in mind before adding new products. Which leads to the next one…

Before adding a new product to the portfolio, always write

up a business case and do sales/cost impact projections. In fact, this should

also be done for any request or change to a product or portfolio.

Product customization is less important that total customer

buying experience. If you make it easy for your customer to buy your product,

you will have more sales.

22-Nov-2019

As of right now, the business is still operating. I do not

know how much longer that will be the case. It continues to limp along, hanging

by a thread.

Stay tuned for further updates…

And, as always, let me know what you think in the comments. Ask questions, tell your story.

If you like my posts, please share them with others and

subscribe to this blog.

Wow, it has been a while since I’ve written anything here.

Things have been busy, to say the least, between my regular job and family. My

oldest started high school marching band as a freshman and her schedule is

brutal! (Translation: Lots of after-school practice, football games, and

marching competitions).

Today we are going to talk about when things don’t go right

in a business, from a finance perspective based on a business I am involved in.

The names have been changed to protect the innocent.

Business History

In March of 2017, a group of former colleagues, with me as a

minor investor, purchased a door manufacturing business. At this point, none of

us had ever been involved in that industry, but we thought that between the

four of us, we could figure everything out and grow the business.

Prior to the purchase, we examined the prior owner’s books

and he seemed to be making decent revenue and profit. We tried to analyze Cost

of Goods Sold (COGS) and Expenses to get a good handle on what our potential

revenue could be.

Because three of us were working full time jobs, the fourth partner, we’ll call him Bob, was going to run the business initially, until we could grow the business enough to hire someone to manage it.

We attempted to get Bob to put together a pro forma operating expense projection, but he kept claiming “he would not be able to accomplish this until he was actually working IN the business and understood everything”. RED FLAG #1 (In hindsight, this should have shut down the deal for us.)

Once we purchased the business, Bob assigned himself a $100,000 per year salary because that was what he “needed” to survive on. We, the other investors, had not begun to understand the business’s key financial benchmarks at this point, so let it slide. RED FLAG #2

After six months or so of this, we begin to realize that our working capital was steadily draining. In addition to Bob arguing against every suggestion the board, (other three investors), would make to improve things, agreeing to implement the suggestions, then never acting on them. We slowly started to realize that even though we all agreed at our initial gathering that this was an investment to grow and either sell it for a profit or, after three years of profit reinvestment, provide cash flow and dividends, Bob was acting as if he was setting up Bob’s Kingdom. He wanted to run the business exactly as the previous owner had run things. RED FLAG #3

We made changes. First, we reduced the salary to $50,000, a

figure more in line with the position. Then we removed him as President. We

attempted to replace him with a salesman we brought on and moved Bob into the

sales role, but since Bob was still involved and also trained the salesman, he

was set up to fail. Bob did not teach him everything and did not say anything

when things slipped through the cracks until after we noticed a couple of

months down the line.

Current Status

The business continues to limp along. We have not put any

more capital into it. Bob occasionally takes out small invoice-secured loans

when the bank account gets too low. He is working at another job and has the

lead employee mostly running the business.

We other investors have mostly given up on expending more

than just a nominal effort to expand the business since no advice given is

followed. We came up with plans and strategies on how to streamline the

business and improve revenue, and presented them as a means to grow the

business, but they didn’t sit well with King Bob, so they went nowhere.

The best I can hope for is that I can harvest some capital

gains from other investments when this business eventually fails so I can

offset the losses on my taxes.

In a future post, I plan to lay out the lessons learned from

this experience and hopefully it will help you, the reader, to avoid some of

our mistakes.

Post in the comments about your things that didn’t go right.

And, as always, let me know what you think in the comments.

Ask questions, tell your story.

If you like my posts, please share them with

others and subscribe to this blog.

Do you ever get to a point where you are feeling overwhelmed

with everything going on in your life? The constant demand from work, the

building up of lots of meaningless little things that put you in a funk? Or

what about a sudden realization that things in your life that you took for

granted are no longer a sure thing?

Well, that has been me for the last few months. I believe it started with my health. As I talked about in a previous post, I was diagnosed with thyroid cancer. And luckily, it was the easily treatable, slow growing kind. Simple solution. Remove the thyroid gland, check for any other abnormalities near it, and carry on.

Or at least so I thought. The surgery was quick and without

complications. No abnormalities observed in the surrounding tissues, most

likely due to such an early diagnosis. When the pathology came back saying that

there was a third tumor growing on the other side of my thyroid gland, my

endocrinologist decided to ablate me with radioactive iodine. This would kill

the remaining thyroid cells and virtually eliminate any chance of thyroid

cancer coming back.

Because he suspected that we might have to go that route, he

did not start me on replacement thyroid hormone medications, choosing to wait

until a decision was made on the radioactive iodine (RAI). I felt fine right up

until I did the RAI. This was approximately 6 weeks post-surgery, which is also

just about the length of time that thyroid hormones live in your body. What

that means is that I had little to no energy and mostly just sat around.

I was able to start the meds a couple of days after the RAI

and I began to feel better. Over the next few weeks the doctor ramped up the

dosages, trying to get my hormone numbers in line. And it worked/is working.

BUT, I have nowhere near the endurance I used to. I normally get up around

05:00, give or take. But by 17:00 – 18:00 in the day, I had no more energy. Now

I am able to last to about 20:00, then it is sit or lay around and nothing

strenuous.

So that was bad enough, but on top of that, my glucose

levels have begun to go a little haywire. I can have normal numbers throughout

the day (120 – 150) & low levels at night (45 – 68), then wake up in the

morning to levels at 245 -280.

The doctor thinks that it may stabilize once we balance my

thyroid hormone levels. It also may be related to a medication change made a few

months ago.

In addition to the medical issues, there has been a lot of

stress at work, which probably magnifies all of my medical issues.

With all of this going on, I did not feel like doing much of

anything extra-curricular. I had a realization that this was my new normal.

There would be no more “go, go, go” and rest on the weekends.

I was depressed.

Now I don’t claim to have a solution for depression, I am

only relating what I am observing.

We took the kids to see Weird Al Yankovic in concert in New

Orleans, that seemed to help. And this week, I had to travel to Dallas to

present at a workshop for a different group in the company for my job. While

there, I had dinner with a buddy I hadn’t seen in twenty-plus years. IT was

good to catch up with him. On top of that, I started to listen to music a

little more. My aural diet has been mostly podcasts and audiobooks for the last

three or four years, so music is a refreshing change, in addition to being

therapy for my soul.

So, what I suggest to you, dear reader, is that if you find

yourself in a similar situation, don’t wait to do some self-therapy…find what

feeds your soul. Take Care of Yourself.

Do you have single family or small multi-family rental properties and need to insure them? Are you a flipper in need of a rehab policy? Visit National Real Estate Insurance Group. Great rates. Coverages you need. Commercial Liability. Monthly Payments, No Financing. Add/Remove Properties as Needed.

And, as always, let me know what you think in the comments.

Ask questions, tell your story.

If you like my posts, please share them with others and

subscribe to this blog.

Today I am going to do a review of Stessa, an online rental

property accounting platform.

But first, a disclaimer:

***This review may contain affiliate links that compensate me for user

registrations of this product.***

As I have detailed in a previous article, I started using Stessa

last year to track accounting for our rental portfolio. Previously, we used

Google Sheets, tracking rental income and expenses for each property on

different tabs. This would involve me going in to the first property’s income

tab, entering the collected rent, then checking all of my receipts and accounts

to verify I hadn’t missed any expenses and adding them to the expense tab for

that property. I set up expense categories and put in a section to summarize

the expenses by category and by month. While not ideal, it insured that someone

at my CPA’s office was not classifying an expense in the wrong category or for

the wrong property. It was not hard to do, just more a matter of remembering to

do it.

Around the middle of 2018, I started seeing advertisements for a product called Stessa on Facebook. As per my SOP, I ignored them, other than taking note of the name. A few weeks after first seeing the ads, I heard an advertisement for it on The Bigger Pockets Podcast. This was more effective, as they pointed out how it was free for rental property owners and individual investors and involved some automation to keep track of your accounting. They also pointed out how the product was developed by real estate investors for real estate investors and the name was “assets” spelled backwards.

I went to the web

site and registered for it. I was able to set up our properties and import

bank & credit card histories to the transactions section, allowing me to

categorize each expenditure. It took maybe 10 minutes to set up two properties.

And, once numbers had been entered, the dashboard populated with portfolio

metrics. Way nicer than my spreadsheets!

Features

Individual tracking for each property:

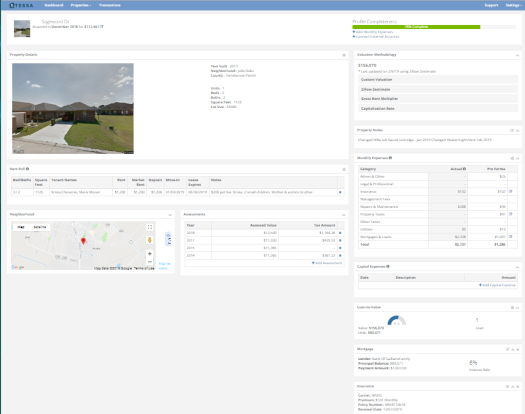

Property Profile

Header – Address, Acquisition Date, and Cost.

Property Details

– (Year built, neighborhood, parish [county, for those of you outside

Louisiana], number of units, bedrooms, bathrooms, square footage, and lot size,

all pulled from Zillow, based on the address.)

Valuation – Provides

for multiple options: Custom Valuation, Zillow Zestimate (automatically polled,

user choice to update property valuation), Gross Rent Multiplier, or Capitalization

Rate.

Rent Roll – Allows

entry of Bed/Baths, Square Feet, Tenant names, Rent, Market Rent, Deposit,

Move-in Date, Lease Expiration Date, and notes.

Property Notes

section – Freeform note space for property.

Monthly Expenses –

Allows for Pro-Forma expense entry and pulls in categorized expenses from the

Transactions section to show actuals compared to Pro-Forma.

Neighborhood –

Shows location on a Google map, with a Walk Score and a Bike Score for the

property.

Assessments –

Pulls in assessed value and property tax amount (I’m assuming from Zillow), and

allows you to add missing assessment/tax details.

Capital Expenses –

Allows for entry of Date, Description, & Amount of Capital Expenditure.

Loan-to-Value –

Shows a chart with LTV percent, Property Value, Debt (principal balance), and

number of loans.

Mortgage – Details

the Lender, Principal Balance, Payment Amount, and Interest Rate.

Insurance –

Displays the Carrier, Premium, Policy Number, and Renewal Date.

Transactions:

As I mentioned above, Stessa

allows you to link bank accounts and credit cards to the Transactions ledger.

It lets you initially import all transactions and gives you the option to

review them to either categorize each one correctly or, in my case, the credit

card I use also has personal charges, so it it allows me to delete those

transactions.

Stessa does not store your credentials on their servers and

use bank-level encryption to secure the transfer of information. It also does

not allow changes to your bank or credit card accounts. It only pulls a copy of

your transaction information.

The Transaction Ledger Menu allows you to review new

transactions, view ALL PROPERTIES transactions, view individual property

transactions, or add a new property.

The main Transaction Ledger display shows all transactions, filtered,

based on the menu selection. It additionally allows you to search by keyword

and/or filter by Date, Category, Amount, or Account.

There is also an export function, allowing you to export

filtered transactions to a *.csv file.

You can manually import *csv and *.qif files from accounting

software, in addition to adding individual transactions by hand, such as

mileage.

Reporting – Reporting is one of the reasons I was interested

in trying out Stessa in the first place. It provides you with standard reports

such as Income Statements, Cash Flow, and Capital Expenditures, with options to

select a date range, property/portfolio, monthly breakout, and whether or not to

show Category Details. The report is downloaded as an Excel file, allowing you

to customize the report title and report formatting, if needed.

The other reporting option I have mentioned before is the

Tax Package. This contains everything needed to hand off to your CPA at tax

time. And it sure makes it easier on me!

The dashboard is the main page you see when logging in on a

computer. It allows you to show the total portfolio or to select individual

properties.

It contains the following sections:

Portfolio Value – Options to see Market or Purchase Value.

Asset Return – Either Appreciation or Levered returns.

Occupancy – Detailed in percent.

Income

Cash Flow

Unit Count

Property Count

Debt – Total

Net Cash Flow – A chart detailed by month & Category

Location – Google map showing all properties in Portfolio

View or a single property in Property View

Compare Properties – Rental Income, Market Value, and Square

Feet. Available in Portfolio View only

Property Highlights – Property picture from Google Street

View, Income, Expenses, LTV, and Occupancy. Available in Property View Only

Summary

I think that Stessa is a great automation tool for rental property accounting. It’s free, cuts down on time spent doing bookkeeping, and makes tax time easier. On top of that, their user support is outstanding! Early on, I identified a couple of bugs and they were fixed within a couple of days. Amazing!

If you are interested in trying out Stessa for your rental properties, please click on the link below:

Do you have cable and/or cable services like phone, tv plus premium channels, and internet? Does it seem like the cost keeps going up? ME TOO! LOL

Read on to see what we did to reduce our costs for these services.

Initial Setup

Our entertainment setup consisted of two Tivos, (1-Premiere

model capable of cable & OTA Reception, 1-Roamio model-cable reception only),

four TVs, (1-LR, 3-BR), two digital signal adapters for the Kids’ bedrooms, two

Firesticks (LR & MBR), VoIP phone from the cable provider, mid-tier cable

TV package with no premium channels, (up to) 150 MB/s internet connection, a

family Netflix subscription (allowing simultaneous logins), Prime Video

(complimentary with Prime account), and a promotional Hulu account for

$0.99/month for a year. Our cable, phone, and internet were all with Comcast.

Our bill has gone up & down depending on what

promotional package we would renegotiate for, but that involved going to the

cable company office, in person, and asking for it, usually after waiting in

line for a while. That was aggravating enough, but the bill would continuously

increase, outside of the changes to promotional status.

We don’t watch a lot of TV. Just a few shows. And we never

watch them live. We have too much other stuff going on. I started to evaluate

our habits after our total bill came off of promotional status, raising the

cost from approximately $137/month to $165/month. Then, for no reason, it went

up to $174/month.

It turns out that most of the shows we watch are either only on a streaming service or show up on Hulu. It should be acceptable to only use streaming services. We decided to get an antenna to pick up local stations. We figured it would be hit-or-miss, because we live between 40-50 miles from the regular broadcast network towers. BUT, if we could get some channels, we could still get news during a storm if the internet goes down.

I discussed the idea with my wife and we decided to get an

antenna and try it out. I researched antennas and almost bought a couple of

different expensive ones, (amplified, slick advertising, etc.), but decided to

start at a lower price point, always having the option to escalate, if needed.

I settled on the GE

Pro Outdoor/Attic Mount Antenna. It claimed to have a range that would

allow us to receive the stations we wanted.

When it arrived, I connected it to the TV in the living room,

(with the antenna sitting on my couch) and scanned for channels. It was able to

pick up around 33 channels!

I then mounted it up in the attic and connected the living

room TV to it, resulting in 38 – 42 stations coming in, depending on the

weather.

I added a signal booster / splitter that would allow me to

connect the other three TVs to the antenna. I was able to hook them up and get

the same channels, so all was well.

The Tivo Premiere is able to receive Over The Air (OTA) signals to the tuner, so we set it up to record all of our broadcast network shows and we can use the Tivo Roamio in our bedroom to watch the recordings via network transfer between the Tivos.

We additionally got Firesticks for each of the kids’ TVs,

allowing them to access Netflix & Hulu on their TVs.

Because we were still using the “Triple-Play Gateway”

modem-router-access point, it would continue to cost us an additional $13/month

in device rental fees. I didn’t like that. Time for more research!

I found a cable modem, (MOTOROLA

24×8 Cable Modem, Model MB7621) that would continue to provide us with the

same speeds we were getting with the Comcast gateway, but it was only a

one-time cost of approximate $70, as opposed to the monthly charge for the

device rental. I got it, hooked it up and was able to configure it online in

less than 10 minutes.

Our plan was to keep the internet. During my research, I

called Comcast and asked about the internet charges, because their website said

normal charges for internet were $71-$80/month, and was told that the price

would indeed be $80/month.

Now that all of the hardware was replaced, I went to the

Comcast office to return all of the equipment. The guy behind the counter said “OK,

we can set you up with a promotional rate of $54.95/month for internet only, at

the current speed you have.” Bingo! This is the same promotional rate they are

offering to new subscribers for twelve months! I was ecstatic!

Cost Reductions

Before

Monthly recurring costs were $174 for TV, phone &

internet = $2,088/year

After

Monthly recurring costs are $55 = $660/year

One-time costs were approximately $240 for the antenna,

splitter/booster, 2 Firesticks, and a cable modem.

Net Savings of $1,188 in the first year (495% ROI) and

continuing savings of $1,428 per year going forward.

Have you or are you thinking about cutting the cord? Let me

know in the comments.

And, as always, let me know what you think in the comments.

Ask questions, tell your story.

If you like my posts, please share them with others and

subscribe to this blog.

This week we are going to go over

some myths regarding taxes for small businesses. I get a newsletter from our CPA

each month that covers tax-related topics. The articles are written by other

people and I am assuming his website subscribes to these articles from a

service.

I found the topic of this one

interesting, so I searched for the title on the web and found the original

author. Here

is the original article, by Juanita Farmer, CPA, of Germantown, Maryland.

There are a lot of myths &

misconceptions around what you can and can’t benefit from with regards to taxes

in the US. Below we are going to cover seven of the most common ones.

***DISCLAIMER

– I am not a CPA and DO NOT Offer tax advice over the internet or otherwise.

Please consult with your CPA for tax advice. This article is for informational

purposes only***

Business start-up costs are the costs incurred prior to the

business actually beginning operation. They range from advertising and travel

to surveys and training. Organizational costs such as these fall under capital

expenditures.

Just like you can amortize depreciation of equipment, when

you start a business, you can amortize some business start-up costs.

You can deduct up to $5000 of business start-up costs and up

to $5000 of organizational costs. For start-up or organizational costs that

exceed $50,000, the $5000 deduction is reduced. The remaining balance must be

amortized.

Overpaying Taxes Makes

You Audit-Proof

From a business perspective, the IRS is only worried about

if your documentation matches your deductions and that your deductions are

legal and legitimate. Properly document expenses and follow the advice of a

good tax accountant to “Audit-Proof” your business.

You Can Take More

Deductions for an Incorporated Business

You don’t need an Incorporated Business to deduct business

expenses. Plus, depending on the corporate entity, you may have more tax and

tax filing burden.

Home Offices are an Audit

Flag

Home offices used to be a common audit flag, but with so many

people now utilizing home offices, the IRS issued a a simplified home office

deduction that is easy to claim, with proper recordkeeping.

No Business Expenses are

Deductible If You Don’t Take a Home Office Deduction

All business expenses such as travel, business supplies,

equipment depreciation, etc. Are deductible, regardless of if you take a home

office deduction or not.

Filing an Extension

Delays Your Tax Payment Due Date By 6 Months

Regardless of whether you file for an extension or not, if

you owe any taxes, payment is due on the original due date, typically around

April 15. All an extension does is allow you a six month extension to this deadline to turn in all

of your paperwork/documentation.

Part-Time Business Owners Can’t Have Self-Employed Pension Plans

Even if you are working a full-time job with 401k benefits

and you start a small business, you can

still set up a SEP-IRA for that small business