The oil and gas industry is in turmoil and service companies, in particular, are reducing their footprint in an attempt to weather the double-pronged attack of oil price wars and pandemic lockdowns.

Until yesterday, I worked for one of those companies, as some of you long-time readers may know.

I received a phone call from my manager, and HR, telling me that due to the current environment, my position was being eliminated.

It is not a bad thing. I only took the position back in January because I was unsure of what I wanted to do when my regional position was eliminated. I figured that they went through a lot of effort to keep me in the company and I didn’t have an immediate alternative plan, so I worked the job in Houston.

Then the pandemic hit and everyone was on lockdown. Luckily, I was able to continue working, from home.

BUT, during this time, I realized that I did not want to go back to Houston for work. We decided that I would continue working, as long as I could do it from home, and as soon as I was told that I needed to show up in Houston, I would resign.

It seems things have worked out for the best, because instead of just resigning, I am leaving with an early retirement severance package!

Because of this, I am now free to explore other opportunities…One will be to continue to be involved in real estate, but to a larger degree. I will continue to invest, but now I am pursuing a realtor’s license.

I will also be available to consult on any innovation projects that might come my way. This will allow me to flex my mental muscle “coming up with cool shit” as a colleague is fond of saying.

I will also look for small businesses that the owners are preparing to retire with no one to take them over. I will only pursue them if they are profitable. It should be easy to make a good deal on something like that when the options are sell at a discount or shut it down.

I want to start out this article by asking, how are you? No, REALLY…How are you holding up with all of this unprecedented turmoil? If any of you readers need to talk, have questions, or need advice, please reach out to me here. (Link will take you to a contact form. Your information will not be shared or used to sell you anything.)

While I am classifying this under Personal Finance, it also has a lot to do with Personal Improvement. We are in the fabled “Interesting Times”. In the midst of a viral pandemic, with an oil price war going on, in addition to the main response in the USA to the pandemic has been to shut down most small businesses. This is not good for individuals nor the economy as a whole. And yes, there have been attempts by the government to provide support, with individual stimulus checks and various SBA (Small Business Association) loans with potential options for loan forgiveness, the implementation was far from ideal. There were large corporations receiving small business loans in the millions of dollars. Some people believe this is the fault of the government. In a way it is, but ultimately, it was left up to the banks who administer these SBA loans to underwrite and approve them. With some understanding of the underwriting process, it seems only natural that the businesses with the best chance of paying back the loans would get approved first and for the largest loan amounts.

OK, now that I have that off of my chest, on to the main topic.

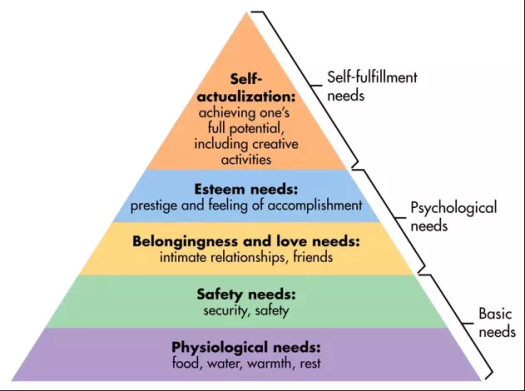

What is your level of Concern?

Where are you with regards to your level of concern? I feel there is a hierarchy, more or less paraphrasing Maslow’s Hierarchy of Needs. I’ll call it Galliano’s Hierarchy of Concern. Depending on your situation, you should be able to relate to the level of concern.

Each step in the pyramid parallels Maslow’s, so technically, it is Maslow’s, just through a different lens.

Survival

At this level of concern, you are just worried if you will live through the virus, if your immediate family will be able to eat, and you will continue to have a place to live.

Employment

This level is fairly obvious, but with a little more. Do you have a job? If you do, is it paying you enough to cover your needs? And if you have a job, is it one that makes you worry about level 1 concerns, like your health and wellbeing?

Savings

The next step up is Savings. Are you able to save enough on a regular basis? Are your current savings enough to carry you through should you become unemployed?

Retirement

This step assumes that you have the previous three steps in hand and under control. It is where you become concerned about retirement. Typically, this step is reached later in life, but not exclusively so. The main questions are “Am I accumulating enough to support me through retirement?” and “How soon can I retire?”.

Reallocation

Similar to the previous step, this step assumes you have the underlying foundation of the other steps under control. Reallocation should be a regular practice for your portfolio to ensure it is optimized for your goals, but in times like these, your concern can also be directed at weathering the volatility and what is the best investment for the current economy.

My advice with all of this, no matter what level of concern you are at, is to take action to improve your current situation. There are no quick fixes, only perseverance of spirit. If you are looking for motivation or direction, checkout my book recommendations. There are more than a few ideas on how to improve your situation.

And, as always, let me know what you think in the comments. Ask questions, tell your story.

If you like my posts, please share them with others and subscribe to this blog.

If you are like a lot of people, you find yourself with a bit of down time thanks to stay at home orders and social distancing keeping people from gathering. I am lucky enough to be able to work from home. With it being a 14 day on, 14 day off rotation, I have had time to add a few skills to my tool belt.

Add something useful to your arsenal that will help you in the future. Some examples are videoconferencing, livestreaming, CRM, Marketing.

Below are some of the things I worked on:

Livestreaming – I learned to use StreamYard to allow me to livestream up to six webcams and screen sharing to multiple locations like YouTube and Facebook. My last two posts have links to the videos. It is a nice platform with professional tools.

Videoconferencing – While I was pretty familiar with videoconferencing, I was not that familiar with Zoom. I was able to learn a bit about it.

CRM – I use HubSpot’s free option for CRM (Customer Relationship Management). Though I previously only used it to track email opens & reads. I learned to manage lists, forms, newsletters, and marketing emails with it. This is going to make managing my local REIA a little easier!

Writing an eBook – As part of digging around in my CRM and learning more about it, I ran across a service that helps you to put together an eBook from existing blog posts to use as a lead magnet. I didn’t like the output, so I decided to tackle the project in earnest from a different direction. Look for it in the near future. He working title is “A Small Business Startup Primer”

What types of skills have you added to your bag of tricks so far?

Let me know in the comments or email me directly.

Be safe and take care!

And, as always, let me know what you think in the comments. Ask questions, tell your story.

If you like my posts, please share them with others and subscribe to this blog.

I did another live stream for my local REIA group and wanted to share it here. The guest is Keith Baker, host of the Private Lender Podcast.

In this video, Keith Baker, Host of The Private Lender Podcast, talks to us about how he got started in private lending, things to watch out for when lending, and his outlook for the future.

Things you will learn in this video:

How Keith got into private lending

How private lending works

Difference between Hard Money Lenders, Private Lenders, and Banks

How Keith screens borrowers

Keith’s “Trademarked” 3Ps Strategy

Why it is good to say no sometimes

Why you should always follow your processes

What a self-directed custodian is

Resources mentioned in this episode:

Sign-In Sheet (Go fill out this form to get on the Group newsletter list)

How are you doing? How are you handling the mis-named “social distancing”? We are going a bit stir-crazy. I am probably more used to the isolation and not being able to go anywhere from when I worked offshore in the oil and gas industry. This is a lot nicer than sitting on a floating rig that you have to fly for one to two hours in a helicopter to reach.

Feel free to reach out if you need to talk to someone. It actually helps with the isolation.

Now, on to the content…

Due to the statewide Stay at Home order here in Louisiana, our local REIA are not able to get together for our monthly meeting. So, I’ve decided to move it online, replacing it with a livestream. Since it covered topics that I think are relevant to a larger audience, I’ve decided to share it with this community, too.

In this video, Tim Blanchard, of Allegiance Home Lending, discusses how mortgage rates work, what the impact is from the Q1 2020 FED Interest Rates on mortgages and regular loans, and gives advice on utilizing SBA Coronavirus relief options.

Things you will learn in this video:

What affects mortgage rates.

What mortgage rates are based on.

What drives a change in mortgage rates.

How Lenders’ Credit Score Criteria have changed in this environment.

SBA Coronavirus relief opportunities for businesses.

Today I’d like to pass on something I have shared in our local REIA group with regards to working with your tenants during this time of crisis, especially if they have recently become unemployed or furloughed.

If you have rentals and have not done so already, it might be a good idea to reach out to your tenants and check in with them. Due to various business shut-downs, lock-down, and stay-at-home measures, they may have become unemployed. Depending on their financial situation, it may make it difficult for them to pay their rent.

Below is a copy of what we sent out to tenants:

Hi, Tenant

How are you? We hope you and your family are staying healthy and getting by at the moment. While I don’t know exactly how the coronavirus situation has impacted you, I’m sure it has not been easy. Personally, my family and I are going a bit stir-crazy, but are taking the down time to ride our bikes and totally redo our landscaping, (who needs the gym, right?)

I imagine you are spending more time more time at home than usual, given the current circumstances. Maintenance people are tough to schedule right now due to safety concerns, but please do not hesitate to reach out if there are any maintenance issues so we can make your your extended time at home more comfortable.

If you have any other needs or issues, again, do not hesitate to contact us.Below is a link to a list of resources that may be helpful during this trying time:

Since we currently cannot conduct eviction proceedings, (and to be honest, this is not the time to be evicting people unless you were already planning or in the process, more on that in a bit), I think it would be best to work with your tenant to see what they can pay, and accept that with the understanding that the balance is still owed. You can work out a repayment schedule over, say, 10 months or so, starting in May. This gives the current craziness time to settle down and should make the payments small enough so that it does not wreck their budget. This assumes your tenant is staying with you long-term.

Additionally, you should get this repayment agreement written up as an addendum to your lease. This will provide a paper trail of it.

***DISCLAIMER*** I am not an attorney and I do not play one on the internet. Please consult your attorney for proper legal phrasing.

Now, if you were already in the process of evicting someone or preparing to, one option you can try is “Cash for Keys”. This is obviously not without cost, but could possibly give you a quicker resolution than waiting to evict them. The way cash for keys works is that you offer the tenant you want to leave a lumps sum dollar value to vacate the property, leaving it in undamaged clean condition, within a certain number of days. You frame it to them as something to help them find a home that better suits them. And, unless there is already a lot of damage to the property, give them back their full deposit to expedite the process. This will help to keep them from damaging the property before leaving.

Merry Christmas! Happy Holidays! Happy Solstice! Happy Hanukkah! Joyous Kwanzaa! Yuletide Greetings! Joyeux Noël! Feliz Navidad! Season’s Greetings! Happy New Year! Joy! Celebrate! Be Merry! And most of all, wishing all of you who read this a new year full of peace and joy!

I’m sitting here between Christmas and New Year’s Day contemplating the future. To paraphrase Game of Thrones, “Change is Coming”.

As many of you know, we decided to start investing in real estate as a buffer to the ups and downs of my chosen industry, Oil and Gas Exploration. I was able to make it through some of those ups and downs in the past, maybe by luck, or because what I was working on was important. At one point, I did take a demotion and worked in the field (offshore, on the rigs, for about a year, but was able to move out of that role and on to greater things.

Which brings us to current times. Things have dipped again.

I usually take the last two to three weeks of the year off since I usually don’t use all of my vacation throughout the year. I was sitting at home and my supervisor called and asked if I was at the office. Since I wasn’t, he asked if I could come in. This told me that something was up because his office is over 100 miles away and if he is at my office, then it must be my turn.

And it was, but with a twist. I was offered a choice between an early retirement package or a rotational position working in Houston.

My darling wife and I contemplated the choices for a couple of days. Ultimately, we decided that it would be best to take the position in Houston. While we would be OK with me not working for a while, ultimately, it was our need of medical insurance that swayed our decision. Speaking of medical insurance, my next article will cover my experience in trying to get a quote for it and the fraud potential inherent in the Louisiana Medicaid Program.

Working a rotational job in Houston would mean finding a place to stay when working and time away from the family, but it also would mean that for two weeks out of every four, I would be off of work and free to do as I please.

This should allow for catching up on projects around the house and more opportunity to generate passive income.

The down side is that I will not be in town for some of the Bayou Real Estate Investor Networking meetings. I will continue to organize them, but will have to rely on other members to host when I cannot attend.

Additionally, if any of you live in or around North Houston / Humble / Kingwood and know of decent rentals at a good price, please contact me!

And, as always, let me know what you think in the comments. Ask questions, tell your story.

If you like my posts, please share them with others and subscribe to this blog.

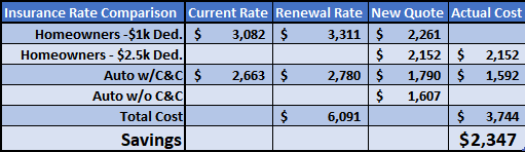

Actual Numbers. Blanks are where numbers were not needed.

Today’s topic is about reviewing your insurance coverages and ensuring that you are properly covered at the best rate. It also touches on customer service and some things that caused me to look for a change.

Isn’t it crazy that it is December already? The end of the year, the end of the decade. Here at the Galliano household we are busy buying Christmas gifts for the family and coordinating our schedules for band concerts, choir concerts, and a birthday.

It is also about paying year-end bills…we have property taxes on our rentals, but that is covered easily by the rent. We also have property taxes on our residence and another property. We can’t do a whole lot about what we are paying on those taxes.

Then there is insurance. Since we paid off our mortgage years ago, we have to purchase homeowners’ insurance outright. AND, since we originally moved into our house right before Christmas, our insurance comes due at Christmas time.

On top of that, our auto insurance is due on 02-Jan-2019. So that totals up to a lot of bills at the end of the year.

The current (as of this writing) agency we use has been providing me with insurance for around 20 years. But I am not happy with them. Over the last four to five years, my “agent of record” has changed at least four times. And the only way I find out about it is if I call with a question. On top of that, when the renewal notices came in this year, they totaled to a little over $6000! I asked for a quote at a lower home value, because the company we are covered with has an auto-escalate policy and increases the coverage value every year, thus increasing the premium. The renewal value was for $291,000. My home is probably worth about $250,000 on a good day.

I also asked for an increased deductible, increasing the deductible from $1000 to $5000. They couldn’t do that. They could only do two percent. So I asked the agent to quote me for coverage on a more accurate home value. Two to three days later, I get a quote for a home value of $232,000. Yes, it was $1000 or so cheaper than the renewal quote, but it was not for the home value that I requested. Because of this, my search for a new provider began.

One of my fraternity brothers offered to give us quotes. In going through that process, we were able to get the coverage we wanted at much lower rates. Between the home and auto coverage, it only cost us $3,744, for a savings of $2,347 between the two. That is almost $200 per month of savings! That will cover a trip to Disneyworld for Mardi Gras! LOL

Tips for Insurance

Below are some tips for getting the most for the least when dealing with insurance:

Review your policies annually to ensure accurate coverage – Make sure you aren’t paying for a home value above the replacement cost of your home

Try to pay your policy in a lump sum – Some providers will give you a discount for paying in full

It pays to shop prices every once in a while

Ensure you have a good relationship with your agent – Find an agency that provides you with a single point of contact and will notify you of any changes

Your home value is not your home replacement value

Depending on the age of your vehicle, you may not need comprehensive and collision insurance

Be in a financial position to be able to pay your policies lump sum

And, as always, let me know what you think in the comments. Ask questions, tell your story.

If you like my articles, please share them with others and subscribe to this site.

Today, we are going to continue where the last article left off. We are going to go over the lessons learned from my experience buying a business with partners. I will list them out with short descriptions. There is no particular order to the list. Any names mentioned other than my own have been changed to protect the innocent…

Lessons

Learned

Partners (The Team) –Our team consisted of four partners. Bob and Carl are the majority investors and took out an SBA loan to acquire the business. John and I are minority partners and not party to the SBA loan. Because Carl, John, and I all have full-time jobs and at the time Bob did not, the plan was that Bob would learn and operate the business until we could afford to put someone else running the business, leaving Bob to pursue his personal interests. See my last article for how that all turned out.

Recommendations:

Be transparent about

individual drivers. Becoming your own boss and becoming wealthy eventually

become competing interests for an entrepreneur.

Professional respect

is critical. Tolerance is listening to every idea quietly. Professional respect

is availability, transparency, punctuality, and preparedness.

Autonomy must be

earned, never assumed in a partnership.

Bad habits are hard

to break in others.

Operating Agreement/Bylaws – Depending on whether you have a Limited Liability Company (LLC) or a Corporation (Co), you should have either an operating agreement or bylaws to govern how the business will be run. In our case, since we had a corporation, we had bylaws. We deliberated on what to include in these bylaws to ensure smooth operations, but did not go far enough. They did not spell out the duties of each partner & role, because we thought that all of us being adults, we would do what was needed to be successful. What we realized was that we each viewed the word through a very personalized lens and what seems obvious to one, (or two, or even three), is not obvious to everyone and if the fourth person feels strongly enough about it, they just will not go along unless forced to. And even then, although begrudgingly agreeing in discussion, they will still fight and obstruct the wishes and decisions of the group. If we had, as a group, decided on the duties for each role and assigned responsibilities for each role to each member of the group, then documented it in the bylaws, it would have made things a lot clearer.

Recommendations:

The operating agreement or bylaws should also include a

defined exit strategy that everyone has agreed to and is committed to

following. It should have defined triggers that initiate the exit strategy.

These triggers should be something that the partners can easily monitor and

measure against.

It should also be spelled out how to handle decisions and

requests. In our case, decisions initially required unanimous board approval.

We amended the bylaws later to only require a two-thirds majority due to the

one partner asking for a solution to a problem, but not liking the board

recommendations, then never implementing the solutions.

Due Diligence – Nowhere near enough due diligence was done on this business or partners. We did not understand enough about how either operated. The revenue the company was making included the previous owner doing work on weekend “off-book” to get jobs out & keep expenses down. It also relied heavily on promotion via owner visits with distributors and their personal relationship. We had no relationships.

Additionally, having a partner who tells the group he agrees

with the intention of not taking any profits for three years, but assigns

himself a $100,000 per year salary and in the first week of operation directly

violates the ground rules we set up for operating the business. We, (the other

three partners), realized that the fourth partner had pursued the investment

deal to set himself up with a kingdom where he was king. #AvoidDat

Recommendations:

Know how the business operates prior to purchase.

Calculate how much revenue you need to make to break even.

Have a budget that takes into account ALL costs to operate.

Unless you are laundering money for drug cartels, whatever

starting capital you have isn’t enough.

That much isn’t enough, either.

Planning to grow? Triple the previous statement.

Financials –While we started out with modest working capital, we had no understanding of our run rate, break-even point, or runway length. In other words, we did not know how much it cost us to operate, how much we needed to make to break even, or how long we could operate with the amount of working capital we had. We eventually figured those things out, but not until it was too late. Also, another point to make, as referenced in a previous article, you have to pay attention to Cash Flow to stay on top of your business finances. We utilized the accrual method of accounting, but did not regularly look at the cash flow reports. Because of this, we would account for interest paid on our loan from the Income Statement (P & L), but did not account for principle repayment in any of our break-even or forecasting exercises until almost two years into the business.

Recommendations:

The person managing the business needs to have a fundamental

understanding of basic accounting and business / financial principals. This is

a KEY point and will lead to many headaches if not followed.

Know your costs to operate, to the penny! AND, make sure you

include labor!

Cash is King! When you run out of working capital, that is

pretty much the end of the business.

Gross margins should be higher than thirty percent. If not,

this will lead to a death spiral for the company.

Sales – The business we purchased operates, (soon to be preterite or past-tense?), conducted sales via a convoluted structure. The products are sold via distributors to building supply centers for builders. So if an end user wants to use our product, they get their builder to point them to their preferred building supply store, where they can look at brochures or in some instances, floor models to decide on what they would like. They then request a quote. That request comes to our operation, is processed, and returned to the building supply store salesperson. That salesperson has limited information on the product nor incentive to sell it.

From our end, we pay a commission to a sales agent to

promote our products to the distributors, who in turn make them available in

building supply stores. This is too far removed from the end buyers and in my

opinion, not an effective spend.

Recommendations:

Agencies DO NOT replace effective sales people! Agencies

represent a large portfolio of products and do not focus on pushing your

product(s) 24/7.

It doesn’t matter what your product is if you and your team

cannot sell the product(s). No sales = No revenue = No profit = bankrupt

company.

It does not matter how much you cut costs or control

spending if you and your team cannot sell the product(s). (See equation above)

Operations / Efficiency – Prior to closing the deal on the business, since Bob was going ot be operating it, we requested that Bob create a budget and document processes for what the business would need to run. He never gave us a budget, nor processes, even after being in the business for a couple of years. His initial excuse was that he had to be working IN the business to understand how the business operated (for processes) and that we, as the board, should be giving him a budget that he could spend. These were two more missed #RedFlags in our journey that should have told us to run, not walk, to the nearest exit. As of today, there are still no documented processes. We kind of have an idea what our budget is through reviewing financials, but we don’t trust the numbers because they are constantly being adjusted. So, we only have an idea, and nothing from Bob. Ultimately, there are still a lot of inefficiencies in the way the business is being run.

Recommendations:

Inefficiency is

expensive and cripples or kills a company. From the start, focus on efficiency

of process, capital, communication, and decision-making.

Be deliberate and

realistic about growth rate. In projections and practice. Year over year

revenue and product volume increases have to be realistic and managed to avoid unmet

expectations and quality issues. It’s nice to have targets, but remember that

you need sales to support targets (see Sales section below). And it is much

easier to have a customer wait for quality than to apologize for a sparkly

piece of crap.

Product Management –This business has about eight main products with practically infinite levels of customization, not counting special-order material types. Every order is a custom order with many options to choose from. There are forty-five different options to choose from when requesting a quote. This leads to decision fatigue and indecision in customers. Ultimately, our quote/win ratio was very low. We suspect that most customers that requested a quote had already decided on something else by the time they received the quote back. Additionally, “Bob” was continuously wanting to add new products to the portfolio because they were the latest hot thing selling.

Recommendations:

Have IP, a unique desirable product, or both. If you have

neither, shoot it in the head, kill the deal, pull the plug, or whatever

euphemism you want to think in. Unless your goal is to be your own boss, then

feel free to limp along for eternity (or until your cash runs out).

Keep or reduce your product line to your top sellers. Based on the Pareto Principle, roughly 80% of your business should come from your top 20% of sales. (Just a note, it will not be exact. This is a rough guideline) So, find out what products make up the majority of your revenue if you already have a large portfolio of products and focus on selling those products. If you only have a few products, keep this idea in mind before adding new products. Which leads to the next one…

Before adding a new product to the portfolio, always write

up a business case and do sales/cost impact projections. In fact, this should

also be done for any request or change to a product or portfolio.

Product customization is less important that total customer

buying experience. If you make it easy for your customer to buy your product,

you will have more sales.

22-Nov-2019

As of right now, the business is still operating. I do not

know how much longer that will be the case. It continues to limp along, hanging

by a thread.

Stay tuned for further updates…

And, as always, let me know what you think in the comments. Ask questions, tell your story.

If you like my posts, please share them with others and

subscribe to this blog.

Wow, it has been a while since I’ve written anything here.

Things have been busy, to say the least, between my regular job and family. My

oldest started high school marching band as a freshman and her schedule is

brutal! (Translation: Lots of after-school practice, football games, and

marching competitions).

Today we are going to talk about when things don’t go right

in a business, from a finance perspective based on a business I am involved in.

The names have been changed to protect the innocent.

Business History

In March of 2017, a group of former colleagues, with me as a

minor investor, purchased a door manufacturing business. At this point, none of

us had ever been involved in that industry, but we thought that between the

four of us, we could figure everything out and grow the business.

Prior to the purchase, we examined the prior owner’s books

and he seemed to be making decent revenue and profit. We tried to analyze Cost

of Goods Sold (COGS) and Expenses to get a good handle on what our potential

revenue could be.

Because three of us were working full time jobs, the fourth partner, we’ll call him Bob, was going to run the business initially, until we could grow the business enough to hire someone to manage it.

We attempted to get Bob to put together a pro forma operating expense projection, but he kept claiming “he would not be able to accomplish this until he was actually working IN the business and understood everything”. RED FLAG #1 (In hindsight, this should have shut down the deal for us.)

Once we purchased the business, Bob assigned himself a $100,000 per year salary because that was what he “needed” to survive on. We, the other investors, had not begun to understand the business’s key financial benchmarks at this point, so let it slide. RED FLAG #2

After six months or so of this, we begin to realize that our working capital was steadily draining. In addition to Bob arguing against every suggestion the board, (other three investors), would make to improve things, agreeing to implement the suggestions, then never acting on them. We slowly started to realize that even though we all agreed at our initial gathering that this was an investment to grow and either sell it for a profit or, after three years of profit reinvestment, provide cash flow and dividends, Bob was acting as if he was setting up Bob’s Kingdom. He wanted to run the business exactly as the previous owner had run things. RED FLAG #3

We made changes. First, we reduced the salary to $50,000, a

figure more in line with the position. Then we removed him as President. We

attempted to replace him with a salesman we brought on and moved Bob into the

sales role, but since Bob was still involved and also trained the salesman, he

was set up to fail. Bob did not teach him everything and did not say anything

when things slipped through the cracks until after we noticed a couple of

months down the line.

Current Status

The business continues to limp along. We have not put any

more capital into it. Bob occasionally takes out small invoice-secured loans

when the bank account gets too low. He is working at another job and has the

lead employee mostly running the business.

We other investors have mostly given up on expending more

than just a nominal effort to expand the business since no advice given is

followed. We came up with plans and strategies on how to streamline the

business and improve revenue, and presented them as a means to grow the

business, but they didn’t sit well with King Bob, so they went nowhere.

The best I can hope for is that I can harvest some capital

gains from other investments when this business eventually fails so I can

offset the losses on my taxes.

In a future post, I plan to lay out the lessons learned from

this experience and hopefully it will help you, the reader, to avoid some of

our mistakes.

Post in the comments about your things that didn’t go right.

And, as always, let me know what you think in the comments.

Ask questions, tell your story.

If you like my posts, please share them with

others and subscribe to this blog.